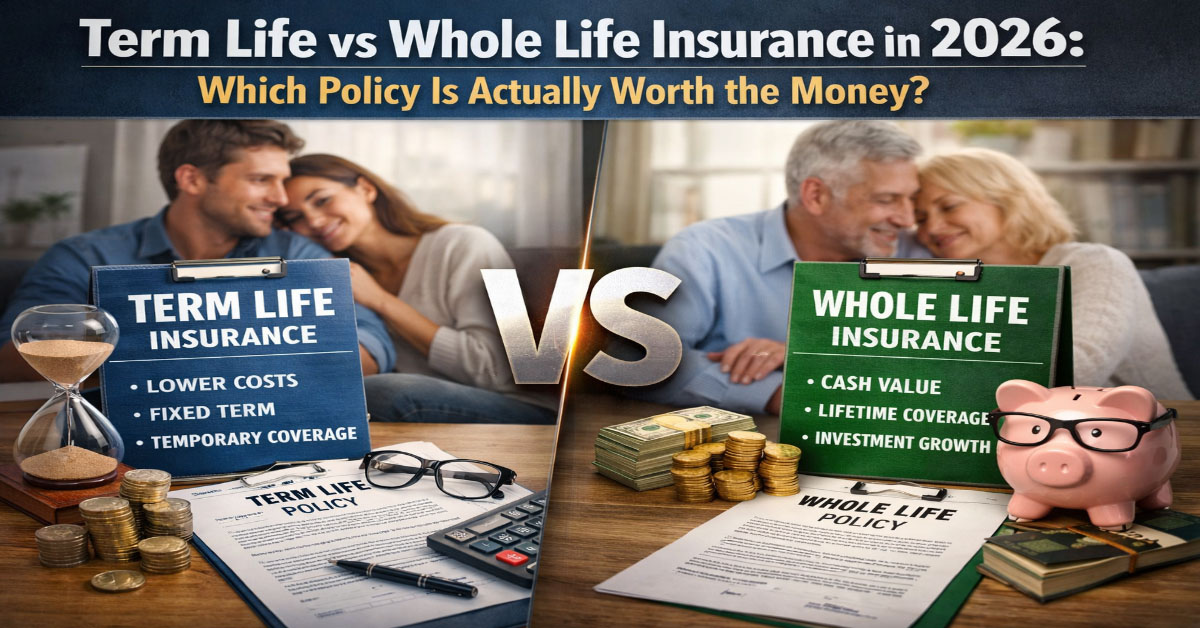

No debate in personal finance generates more heat and less light than the comparison between term and whole life insurance. On one side, prominent financial voices characterize whole life insurance as one of the worst financial products ever sold. On the other side, insurance professionals argue that permanent coverage provides irreplaceable benefits that term insurance cannot match. Both camps contain elements of truth. The full picture is more nuanced than either side typically presents.

The right choice depends on your specific financial situation, insurance purpose, tax profile, estate planning needs, and time horizon. This guide gives you the honest, complete analysis to make that determination for yourself, including the math most articles are afraid to show and the specific legitimate use cases for each product type.

In This Article

- Term Life Insurance: How It Works

- Whole Life Insurance: How It Works

- The Cost Comparison: The Numbers Are Stark

- The Cash Value Reality

- Buy Term Invest the Difference: The Math

- When Whole Life Genuinely Makes Sense

- When Term Is Clearly the Better Choice

- Universal Life and Other Permanent Options

- The Agent Incentive Problem

- Making the Decision for Your Situation

Term Life Insurance: How It Works

Term life insurance is the simplest form of life insurance: you pay a premium for a defined period and if you die during that period, your beneficiaries receive the death benefit. If you outlive the term, the policy expires with no value. There is no cash accumulation, no investment component, and no complexity. The coverage period is fixed at the outset: 10, 15, 20, 25, or 30 years, with 20 years being the most common choice for families with young children who need protection through the years of highest financial obligation.

The premium is set at the time of issue based on your age, health, the coverage amount, and the term length, and is guaranteed level for the entire term period with most policies. A healthy 35-year-old purchasing a 20-year, $500,000 term policy locks in the premium for 20 years regardless of any health changes that occur during that period. The insurer cannot raise the rate or cancel the policy during the term as long as premiums are paid on time.

After the initial term expires, most policies offer a conversion option allowing conversion to permanent coverage, or a renewal option extending coverage at a significantly higher premium reflecting the policyholder's current age. These post-term options are generally expensive and are rarely used as primary long-term strategies. The intended design is that the coverage need no longer exists when the term expires: the mortgage is paid down or off, the children are financially independent, and sufficient wealth has accumulated to be largely self-insuring.

Whole Life Insurance: How It Works

Whole life insurance provides permanent, lifelong death benefit protection as long as premiums are paid. Unlike term insurance that expires at a defined date, a whole life policy that has been properly maintained remains in force regardless of how long the policyholder lives. The death benefit is guaranteed to be paid whenever death occurs, whether that is at age 55 or age 95.

The second component of whole life insurance is the cash value: a savings component that accumulates within the policy over time. A portion of each premium payment, after deducting for the insurance cost and administrative expenses, is credited to the cash value account. The insurer guarantees a minimum growth rate on this cash value, typically 2 to 4 percent depending on current interest rates, and participating policies from mutual insurance companies may also credit additional non-guaranteed dividends that enhance growth above the guaranteed floor.

The cash value belongs to the policyholder in the sense that it can be borrowed against or the policy can be surrendered for its cash value. Policy loans against the cash value carry an interest charge and are not required to be repaid, though unpaid loans reduce the death benefit available to beneficiaries. Surrendering the policy terminates the coverage and returns the cash value minus any outstanding loans and applicable surrender charges in early policy years.

The Cost Comparison: The Numbers Are Stark

The most immediately visible difference between term and whole life is the premium. For equivalent face amounts, whole life premiums are dramatically higher than term life premiums, typically by a factor of 10 to 20 times. This is not a slight cost difference. It is a categorical financial difference that fundamentally changes every element of the analysis.

Cost Comparison: $500,000 Coverage, Healthy 35-Year-Old Male Non-Smoker

The premium difference must be understood in the context of what each product provides. The term policy purchaser is buying pure death benefit protection for a defined period. The whole life purchaser is buying permanent death benefit protection plus a forced savings mechanism in the form of the cash value accumulation. Whether the whole life package represents good value depends entirely on whether the cash value growth is competitive with alternative investment vehicles at the same risk level, after accounting for the true cost of the insurance component embedded in the whole life premium.

The Cash Value Reality

The cash value is the central selling point of whole life insurance and the element most subject to both enthusiastic overselling and justified criticism. A rigorous analysis of what cash value actually delivers is essential to making an informed decision.

Guaranteed whole life cash value growth rates in 2026 typically run 2 to 4 percent on the cash value balance. However, the actual internal rate of return on your total premium dollars is lower because a significant portion of each premium covers the mortality cost and administrative expenses before anything reaches the cash value account. In the early policy years, the surrender value is substantially less than the total premiums paid. Early policy surrenders or lapses result in a significant financial loss relative to total premiums contributed, which is why agent commissions are highest in the early years and the most common adverse outcome for whole life policyholders is buying a policy and then surrendering it within the first several years.

Participating whole life policies from mutual companies may credit non-guaranteed dividends in addition to the guaranteed growth rate. These dividends have historically been paid consistently by financially strong mutual insurers, but they are not contractually guaranteed and can be reduced or eliminated if the company's investment performance or claims experience deteriorates. Projections that assume current dividend rates will continue indefinitely are reasonable illustrations but not contractual commitments.

Buy Term and Invest the Difference: The Honest Math

The buy-term-and-invest-the-difference analysis is the standard critique of whole life insurance and is based on a straightforward calculation worth presenting honestly. Using the numbers above: a 35-year-old chooses between a $500,000 whole life policy at $500 per month and a $500,000 20-year term policy at $30 per month. The monthly premium difference is $470. If that $470 per month is invested in a diversified equity index fund, what does it grow to over various time horizons at a 7 percent average annual return?

After 20 years: $470 per month at 7 percent annual return compounds to approximately $259,000. After 30 years: approximately $587,000. After 40 years: approximately $1,215,000. The whole life policy after 30 to 40 years of premiums would typically have a cash surrender value in the range of $200,000 to $350,000 for a $500,000 policy purchased at 35, depending on the specific carrier and dividend history.

The term-plus-investment strategy produces substantially more wealth accumulation by this analysis. However, the analysis contains important assumptions: the investor actually invests the difference rather than spending it, they have access to tax-advantaged accounts, their risk tolerance supports equity investment, and they outlive their term policy. None of these is guaranteed, which is why the analysis is not as definitively conclusive as its advocates sometimes present it.

When Whole Life Insurance Genuinely Makes Sense

Despite the mathematical disadvantage in most accumulation scenarios, specific circumstances exist where whole life provides genuine and non-replicable value.

Estate liquidity planning for high-net-worth individuals is the clearest legitimate use case. For estates where significant illiquid assets like a family business or real estate are held, the permanent death benefit provides estate liquidity that allows heirs to pay estate taxes without being forced to sell assets at distressed prices on a rushed timeline. This need does not expire at age 65, which is why term insurance cannot serve this purpose as effectively.

Business buy-sell agreements funded by life insurance require permanent coverage because the need for the business continuity arrangement does not end after a defined term. If two business partners agree that the surviving partner will purchase the deceased partner's business interest, that need persists as long as the business exists. A term policy that expires before one partner dies leaves the buy-sell arrangement without funding.

Special needs planning for parents of children with permanent disabilities who will require financial support throughout their lives represents another legitimate permanent insurance need. The child's financial dependency does not resolve when the parent reaches retirement age. A permanent policy ensures the financial support structure survives regardless of when the parent dies.

For very high-income individuals who have maximized contributions to 401(k), Roth IRA, HSA, and other tax-advantaged vehicles and are seeking additional tax-sheltered savings, the whole life cash value provides another vehicle for tax-deferred accumulation. This applies to a narrow segment of the population but is a legitimate use case for that segment.

When Term Is Clearly the Better Choice

For the majority of Americans in the wealth accumulation phase of life, term life insurance is the appropriate choice. The need for death benefit protection is time-limited: the financial vulnerability that life insurance protects against, primarily the loss of income and the financial disruption that would cause for dependents, is highest when children are young and financial obligations like mortgages are largest. These vulnerabilities diminish over time as children grow up, mortgages are paid down, and investment portfolios grow toward self-insurance levels.

Anyone who has not yet contributed maximum annual amounts to available 401(k), Roth IRA, and HSA accounts should not consider whole life insurance as a savings vehicle. The tax advantages, flexibility, and historical returns of index fund investing through tax-advantaged accounts exceed whole life cash value growth in the vast majority of real-world scenarios for people with access to these programs. The buy-term-invest-the-difference strategy requires the investment discipline to actually invest consistently, which is a meaningful behavioral challenge, but the mathematical case for it is compelling when that discipline is present.

The Agent Incentive Problem

Understanding the economic incentive structure that shapes life insurance recommendations is essential for evaluating the advice you receive. Life insurance agents are compensated through commissions that are substantially higher for permanent insurance products than for term insurance. A typical whole life policy generates a first-year commission equal to 50 to 110 percent of the first year's premium. A term life policy generates a first-year commission of 40 to 70 percent of the first year's premium. On an absolute dollar basis, the commission difference is enormous given that whole life premiums are 10 to 20 times higher than term premiums for the same death benefit amount.

This does not mean every agent who recommends whole life is acting improperly. Legitimate use cases for permanent insurance exist and good agents serve them appropriately. But the commission structure creates a systematic bias that every consumer should be aware of when receiving life insurance recommendations from a commissioned agent. If an agent recommends whole life without thoroughly exploring your specific estate planning, business planning, or special needs planning situation that would justify it, healthy skepticism about that recommendation is warranted.

Making the Decision for Your Situation

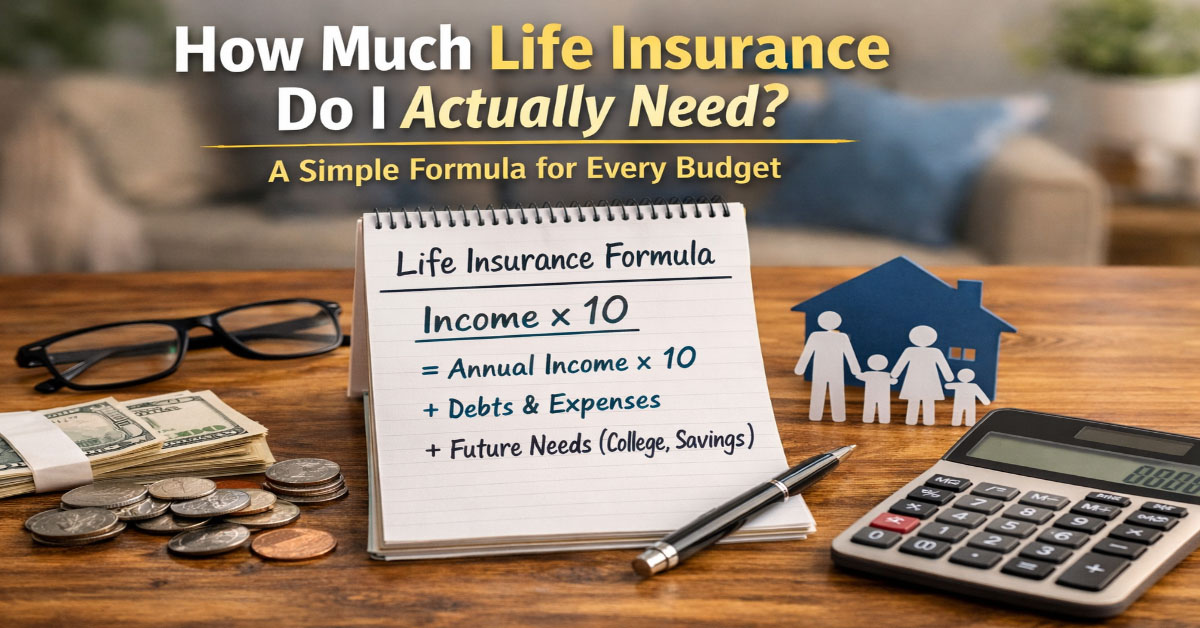

The decision framework is straightforward for most households. If your primary goal is protecting your family's financial security during your working years at the lowest possible cost, buy term coverage for 10 to 12 times your annual income and invest the premium difference in tax-advantaged accounts. If you have permanent insurance needs due to estate planning, business continuity, special needs dependents, or the specific tax-sheltering use case, evaluate permanent options with a fee-only financial planner who has no commission incentive in the recommendation.

The term length decision should match your longest remaining financial obligation. If you have a 28-year mortgage and children who will be financially independent in 22 years, a 30-year term provides comprehensive protection with a small premium buffer. A 20-year term leaves an 8-year gap between policy expiration and mortgage payoff that may matter depending on how quickly your savings accumulate during those 20 years.

The Life Insurance Application and Underwriting Process

Understanding what happens between submitting a life insurance application and receiving your policy approval helps you prepare effectively, avoid surprises, and set accurate expectations for the timeline and outcome. The underwriting process for term life insurance has become significantly more streamlined in recent years, with many carriers now offering accelerated underwriting that can approve a policy in days rather than weeks for qualifying applicants.

The application collects information about your health history, family medical history, tobacco and alcohol use, occupation, income, aviation or hazardous activity participation, and the amount and purpose of coverage you are seeking. For traditional underwriting, this is followed by a paramedical exam: a trained medical professional visits your home or office to collect height, weight, blood pressure, pulse, and a blood and urine sample. Results are reviewed by the insurer's underwriting team along with prescription history from database sources and your driving record.

Based on underwriting results, you are assigned to a risk class: preferred plus, preferred, standard plus, standard, or substandard table ratings for elevated risk profiles. The risk class determines the premium you are offered. If you qualify for a better risk class than your initial estimate, you pay a lower premium than quoted. If underwriting reveals a health condition that increases your risk, you may be offered coverage at a higher premium than initially estimated or declined for coverage in rare cases.

Accelerated underwriting programs, now available from most major carriers for applicants under 60 seeking coverage under $1,000,000 to $2,000,000, use algorithmic review of medical database records, prescription history, and driving record to approve policies without a physical exam. These programs can produce approval decisions in as little as 24 to 72 hours. For healthy applicants with clean records, accelerated underwriting offers the convenience of no exam with competitive pricing. Applicants with health conditions or complex profiles may receive better risk class assignments through traditional full underwriting that includes a physical exam and more comprehensive medical history review.

Naming Beneficiaries: The Most Important Decision After Buying Coverage

The beneficiary designation on a life insurance policy determines who receives the death benefit when the insured dies. This designation supersedes any instructions in a will. It is one of the most consequential financial decisions a policyholder makes, and yet it is also one of the most commonly overlooked after the initial policy purchase.

Every life insurance policy should have a primary beneficiary and at least one contingent beneficiary designated. The primary beneficiary receives the death benefit if they are alive at the time of the claim. The contingent beneficiary receives the benefit if the primary beneficiary has predeceased the insured. Without a contingent beneficiary designation, the benefit would pass to the insured's estate if the primary predeceases them, which can trigger probate, creditor claims, and estate taxes that undermine the purpose of the coverage.

Review your beneficiary designations after every major life change: marriage, divorce, birth of a child, death of a named beneficiary, or significant change in family financial circumstances. Outdated beneficiary designations that still name an ex-spouse are an unfortunately common and easily preventable error that causes significant distress to surviving family members. Contact your insurer directly to update beneficiary information rather than relying on a will or other estate document, since the beneficiary designation on the policy itself is the legally controlling document.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.