The single most important decision in buying life insurance is not which company to use, what type of policy to choose, or how long the term should be. It is how much coverage to buy. Too little coverage fails the people who depend on you when it matters most. Too much coverage means paying premiums for protection beyond what your family actually needs. Getting this number right is the foundation of any life insurance decision.

This guide walks through every major calculation methodology, explains what factors actually drive the number for your specific situation, and provides a framework for arriving at a coverage target that genuinely reflects your household's financial reality rather than an arbitrary rule of thumb applied without context.

In This Article

- What Life Insurance Coverage Is Actually Replacing

- The Income Multiplier Rules of Thumb

- The DIME Method: A More Precise Approach

- The Human Life Value Approach

- Factors That Push Your Number Higher

- Factors That Allow a Lower Coverage Amount

- Two-Income Household Considerations

- Coverage for a Non-Working Spouse

- Accounting for Existing Coverage

- When to Review and Adjust Your Coverage

What Life Insurance Coverage Is Actually Replacing

Life insurance replaces the financial contribution that a person would have made to their household if they had lived. Understanding precisely what that contribution consists of helps you size the coverage more accurately than any general rule of thumb can.

For an income-earning spouse, the primary financial contribution is their ongoing salary or business income. But the total financial contribution extends beyond income to include the employer-sponsored benefits they would have provided, particularly health insurance, which may have a replacement cost of $15,000 to $25,000 per year for a family that must now purchase coverage individually. It also includes any debt obligations co-signed with the deceased that must now be serviced from the surviving spouse's income alone.

For a non-earning spouse who manages the household and cares for children, the financial contribution is less immediately obvious but substantial when quantified. Childcare for young children costs $15,000 to $40,000 per year depending on location and age. Household management tasks including cooking, cleaning, scheduling, transportation, and eldercare coordination have real replacement costs. The death of a non-earning spouse can require the earning spouse to significantly reduce work hours or take extended leave, directly affecting income, not just increase spending on replacement services.

The Income Multiplier Rules of Thumb

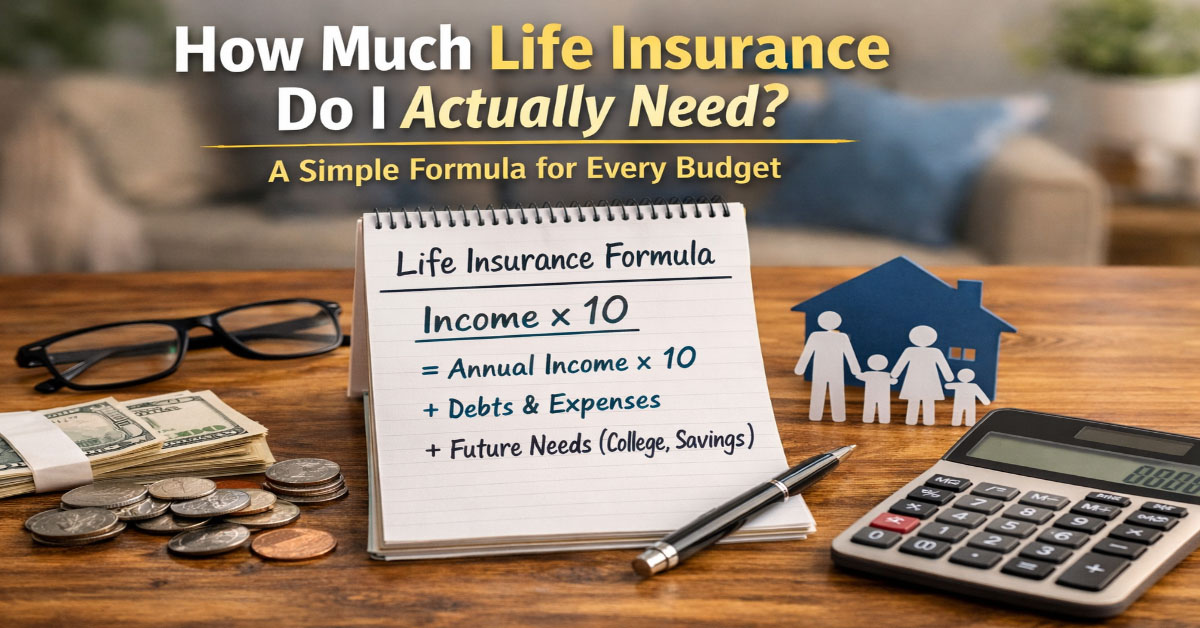

The most widely used starting point for life insurance coverage sizing is the income multiple: a simple formula that multiplies your current annual income by a factor to arrive at a coverage target. The most common guidance is to carry coverage equal to 10 to 12 times your annual gross income. At $80,000 per year in income, this produces a coverage target of $800,000 to $960,000.

The income multiple is a reasonable first approximation for many middle-income households with typical financial profiles. Its simplicity is its primary advantage. Its primary limitation is that it does not account for specific large obligations or assets that differ meaningfully between households. A family with a $600,000 mortgage needs more coverage than a family with no mortgage at the same income level. A family with substantial investment assets providing income replacement capacity needs less coverage than a family with no savings at the same income level. The income multiple misses these differences entirely.

Despite its limitations, the income multiple is a useful sanity check and starting point. If your current coverage is significantly below 10 times your annual income and you have young children and a mortgage, you almost certainly have a coverage gap regardless of your specific financial details. The more precise methods below can refine the target, but the income multiple quickly identifies households that are clearly underinsured.

The DIME Method: A More Precise Approach

The DIME method produces a more individualized coverage estimate by building up from four specific financial categories that represent the most significant financial obligations your death would create or accelerate for your family.

D stands for Debt. Add up all outstanding debt excluding your mortgage: car loans, student loans, credit card balances, personal loans, and any other obligations your family would need to service or pay off after your death. This figure represents the immediate debt obligations your life insurance should be able to eliminate so your surviving family is not burdened by debt payments at the same moment they are managing without your income.

I stands for Income replacement. Multiply your annual income by the number of years until your youngest child will be financially independent, typically age 22 to 25. If you earn $90,000 and your youngest child is two years old, the income replacement component is approximately $90,000 times 23 years equals $2,070,000. This is the amount that, if invested conservatively, could generate your annual income for your family during the years when they most need it. Some financial planners use a slightly different calculation based on the present value of the income stream rather than the simple multiplication, which produces a somewhat lower figure.

M stands for Mortgage. Add your current outstanding mortgage balance. Your death benefit should be sufficient to pay off the mortgage entirely, eliminating the largest single monthly expense your surviving family faces and providing them with housing security that does not depend on continued income.

E stands for Education. Estimate the total future education costs for all children, including anticipated college costs and any private school costs for younger children. Current college cost estimates of $35,000 to $80,000 per year for a four-year degree at in-state public versus private institutions provide a starting point, though families with strong college preferences should use cost estimates appropriate for their target institutions.

The sum of D plus I plus M plus E produces a coverage target that reflects your specific financial obligations. For many middle-class families with young children and a mortgage, the DIME calculation produces a target of $1,500,000 to $2,500,000, a figure that seems large but often corresponds to a monthly premium of $60 to $120 for a healthy adult in their 30s at a 20-year term.

The Human Life Value Approach

The Human Life Value method calculates the economic value of a person's remaining working life based on current earnings, expected earnings growth, working years remaining, and a discount rate that converts future earnings to a present value. This approach is more sophisticated than the income multiple and more theoretically grounded than the DIME method, but it also requires more assumptions that are inherently uncertain.

The basic HLV calculation for a 38-year-old earning $100,000 per year, expecting 2 percent annual raises, planning to work until 67, and using a 5 percent discount rate produces a present value of future earnings of approximately $1,500,000 to $1,800,000. This represents the maximum economically rational life insurance coverage amount on pure income replacement grounds. The HLV approach is more commonly used by financial planners and insurance professionals doing detailed needs analysis than by individual purchasers, but understanding it helps contextualize why coverage targets of $1,000,000 to $2,000,000 are not excessive for middle-income households in their 30s and 40s.

Factors That Push Your Coverage Target Higher

Several specific circumstances warrant coverage above what the standard rule-of-thumb calculations suggest. Young children, particularly those many years from financial independence, extend the income replacement need significantly and should push the coverage target higher. A mortgage balance that represents a large percentage of your coverage calculation, combined with a surviving spouse whose income alone would not service the mortgage, suggests carrying coverage large enough to eliminate the mortgage entirely. Special needs children or dependents with permanent care requirements represent ongoing financial obligations that do not diminish with time and that may require coverage lasting beyond a typical 20-year term. High debt levels outside the mortgage reduce the family's financial resilience and should be explicitly included in coverage calculations rather than being assumed away.

Factors That Allow a Lower Coverage Amount

Substantial existing savings and investment assets that could be liquidated to replace lost income reduce the pure coverage need. A family with $500,000 in liquid investments that could generate $25,000 per year in income can reduce their coverage target by approximately $500,000 compared to a family with no savings. A high-earning, financially resilient surviving spouse whose income alone could substantially cover household expenses reduces the income replacement need. Ownership of real estate beyond the primary residence that generates rental income provides ongoing cash flow that reduces the life insurance coverage need. An expected inheritance or other wealth transfer that is reliable and quantifiable can also factor into the calculation, though such expectations should be treated conservatively given the uncertainty of timing and amount.

Two-Income Household Considerations

For two-income households, the life insurance decision is symmetric: each income earner needs coverage to protect the household against the loss of their specific contribution. The starting point is calculating the coverage target for each partner independently rather than treating the household as a unit with a single coverage number. Each partner's income, debt obligations, and financial contribution to shared household costs should be calculated separately.

The calculation for each partner should include the household's shared obligations that would fall entirely on the surviving partner's income: mortgage, childcare, vehicle payments, and ongoing living expenses. Even if both partners earn similar incomes, the loss of either income creates a financial burden on the survivor that the remaining income may not fully offset, particularly in the near-term period of grief and adjustment before the survivor has had time to make structural changes to the household's financial arrangements.

Coverage for a Non-Working Spouse

Non-earning spouses are systematically underinsured because the financial value of their contribution is less immediately visible than a paycheck. The death of a non-earning spouse who is the primary caregiver for young children creates immediate, large, and ongoing costs for the surviving earning spouse. Childcare for two young children can easily cost $30,000 to $60,000 per year. Household management tasks must either be outsourced at significant cost or handled by the earning spouse, potentially requiring reduced work hours that affect income and career progression. Grief and family disruption often require taking extended unpaid leave.

A commonly cited guideline for non-earning spouse coverage is $400,000 to $750,000, representing the present value of the childcare and household management contributions over the years until the youngest child reaches independence. While less quantitatively precise than income replacement coverage, this range provides meaningful financial protection for the surviving family at a premium that is manageable for most households.

Accounting for Existing Coverage

Most people have some existing life insurance through their employer's group benefit program. Standard employer group life insurance provides coverage equal to one to two times annual salary, with a typical maximum benefit of $50,000 to $200,000 depending on the employer. This coverage should be included in your total coverage calculation but treated conservatively because group coverage is not portable: if you change employers or lose your job, the coverage ends. Coverage needs typically continue through the years of highest financial obligation regardless of employment status, which is why personal term policies that you own and control are important even for employees with meaningful group benefits.

When to Review and Adjust Your Coverage

Life insurance coverage needs change over time, and the policy you purchased at 30 may not be optimal at 40. Major life events that should trigger a coverage review include the birth or adoption of a child, purchase of a home or significant increase in mortgage balance, substantial change in income for either partner, death or disability of a dependent, significant accumulation of savings that reduces the coverage need, and approaching the end of a term policy period when a renewal or replacement decision must be made.

A regular annual review of your coverage level against your current financial obligations, current income, and current assets takes about 30 minutes and ensures that your coverage target remains accurately aligned with your household's actual financial exposure. The most common outcome of such reviews is discovering that coverage levels set during an earlier life stage have not been updated to reflect increased obligations or, conversely, that the financial picture has improved enough to allow a modest reduction in coverage at the next renewal.

The Life Insurance Application and Underwriting Process

Understanding what happens between submitting a life insurance application and receiving your policy approval helps you prepare effectively, avoid surprises, and set accurate expectations for the timeline and outcome. The underwriting process for term life insurance has become significantly more streamlined in recent years, with many carriers now offering accelerated underwriting that can approve a policy in days rather than weeks for qualifying applicants.

The application collects information about your health history, family medical history, tobacco and alcohol use, occupation, income, aviation or hazardous activity participation, and the amount and purpose of coverage you are seeking. For traditional underwriting, this is followed by a paramedical exam: a trained medical professional visits your home or office to collect height, weight, blood pressure, pulse, and a blood and urine sample. Results are reviewed by the insurer's underwriting team along with prescription history from database sources and your driving record.

Based on underwriting results, you are assigned to a risk class: preferred plus, preferred, standard plus, standard, or substandard table ratings for elevated risk profiles. The risk class determines the premium you are offered. If you qualify for a better risk class than your initial estimate, you pay a lower premium than quoted. If underwriting reveals a health condition that increases your risk, you may be offered coverage at a higher premium than initially estimated or declined for coverage in rare cases.

Accelerated underwriting programs, now available from most major carriers for applicants under 60 seeking coverage under $1,000,000 to $2,000,000, use algorithmic review of medical database records, prescription history, and driving record to approve policies without a physical exam. These programs can produce approval decisions in as little as 24 to 72 hours. For healthy applicants with clean records, accelerated underwriting offers the convenience of no exam with competitive pricing. Applicants with health conditions or complex profiles may receive better risk class assignments through traditional full underwriting that includes a physical exam and more comprehensive medical history review.

Naming Beneficiaries: The Most Important Decision After Buying Coverage

The beneficiary designation on a life insurance policy determines who receives the death benefit when the insured dies. This designation supersedes any instructions in a will. It is one of the most consequential financial decisions a policyholder makes, and yet it is also one of the most commonly overlooked after the initial policy purchase.

Every life insurance policy should have a primary beneficiary and at least one contingent beneficiary designated. The primary beneficiary receives the death benefit if they are alive at the time of the claim. The contingent beneficiary receives the benefit if the primary beneficiary has predeceased the insured. Without a contingent beneficiary designation, the benefit would pass to the insured's estate if the primary predeceases them, which can trigger probate, creditor claims, and estate taxes that undermine the purpose of the coverage.

Review your beneficiary designations after every major life change: marriage, divorce, birth of a child, death of a named beneficiary, or significant change in family financial circumstances. Outdated beneficiary designations that still name an ex-spouse are an unfortunately common and easily preventable error that causes significant distress to surviving family members. Contact your insurer directly to update beneficiary information rather than relying on a will or other estate document, since the beneficiary designation on the policy itself is the legally controlling document.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.