Something unusual has been happening in the life insurance market in 2026. According to data from Empathy, a bereavement and end-of-life support platform, searches for life insurance terms have surged by 83 percent compared to the prior year. Insurance agents and direct carriers report inquiry volumes significantly above historical norms. Policy application rates are up. The demand surge is real, broad-based, and driven by several converging factors that reflect how Americans are thinking about financial security, mortality, and family protection in the current environment.

This guide explains exactly what is driving the surge, what first-time life insurance buyers most commonly misunderstand, how to navigate the purchase process efficiently, and how to get the right amount of coverage at the most competitive available rate. Whether you are shopping for the first time, reconsidering an existing policy, or trying to understand why this market shift is happening, this guide covers everything you need to know.

In This Article

- What Is Driving the 83 Percent Demand Surge

- Who Is Buying Life Insurance in 2026

- Life Insurance Basics Every First-Time Buyer Needs

- How Much Coverage Do You Actually Need

- Term vs Whole Life: The Quick Summary

- The Application and Underwriting Process

- What Life Insurance Actually Costs in 2026

- How to Get Coverage Quickly

- Common First-Time Buyer Mistakes

What Is Driving the 83 Percent Demand Surge

Several converging factors explain the dramatic increase in life insurance demand that emerged in late 2025 and continued through 2026. Understanding these drivers helps contextualize why this moment represents something more than a statistical fluctuation and why the behavior change appears likely to persist.

Lingering Mortality Awareness from the Pandemic

The COVID-19 pandemic fundamentally changed how many Americans think about unexpected death in ways that are still influencing financial behavior years later. Millions of families experienced the sudden loss of a breadwinner without adequate financial preparation and witnessed firsthand the economic devastation that an uninsured death can produce. The behavioral impact of that collective experience, while fading, continues to drive insurance purchase decisions that would previously have been deferred indefinitely.

Rising Interest Rates Making Term Life More Affordable in Some Segments

Interest rate dynamics affect life insurance pricing through the insurer's investment return assumptions. In a higher-rate environment, insurers can earn more on the premiums they hold before paying claims, which allows more competitive term life pricing in some duration segments. While this is one factor among many, it has contributed to competitive pricing for certain policy types that has attracted price-sensitive buyers who previously found premiums prohibitive.

Growing Awareness of Coverage Gaps

Financial literacy content across digital platforms has significantly increased consumer awareness of common coverage gaps, including the inadequacy of employer-provided group life insurance (typically one to two times annual salary, far below recommended levels), the gap between a family's financial needs and actual coverage, and the difference between what coverage actually costs and what people assume it costs. Surveys consistently find that Americans overestimate the cost of life insurance by a factor of three to five, and correcting this misperception is directly driving purchase activity among people who assumed coverage was unaffordable.

AI-Powered Application Tools Reducing Friction

The emergence of AI-assisted life insurance comparison and application tools has dramatically reduced the friction in the purchase process. What previously required multiple agent meetings, extensive paperwork, and weeks of waiting for underwriting decisions can now be completed entirely online in many cases. Accelerated underwriting programs that process applications algorithmically without requiring a physical medical exam have made coverage accessible to buyers who would have abandoned the traditional process.

Life Insurance Demand and Pricing: 2026 Data

Who Is Buying Life Insurance in 2026

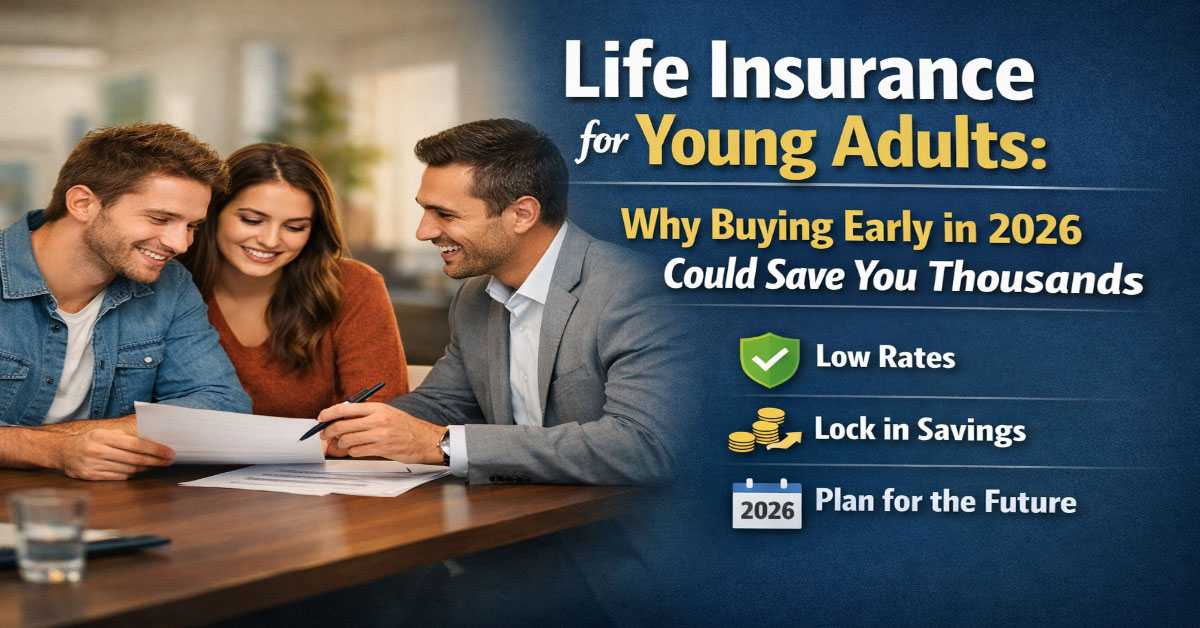

The demand surge is not uniformly distributed across demographics. Data from carriers and aggregators shows disproportionate growth in several specific segments. Millennials aged 30 to 44 represent the largest growth segment, driven by new family formation, mortgage acquisition, and the growing realization that employer group coverage provides inadequate income replacement for a household that has taken on financial commitments based on dual incomes. Parents with young children are buying in the highest absolute numbers, motivated by the concrete thought experiment of what their family would face financially if either parent died unexpectedly.

Single-income households and households where one partner has significantly higher income than the other are another growth segment. The financial modeling of what happens when the primary earner dies is stark: mortgage, childcare, education costs, and daily living expenses continue while the income funding them disappears. Term life insurance at $25 to $35 per month for $500,000 in coverage for a healthy 35-year-old is, for most of these households, among the highest-return financial decisions available given the ratio of protection provided to premium cost.

Life Insurance Basics Every First-Time Buyer Needs

Life insurance pays a death benefit to your designated beneficiaries if you die while the policy is in force. The death benefit is generally income tax-free to the recipient. The beneficiaries can use the money for anything: mortgage payoff, replacement of lost income, childcare and education costs, debt repayment, or simply maintaining their standard of living during a period of grief and financial transition.

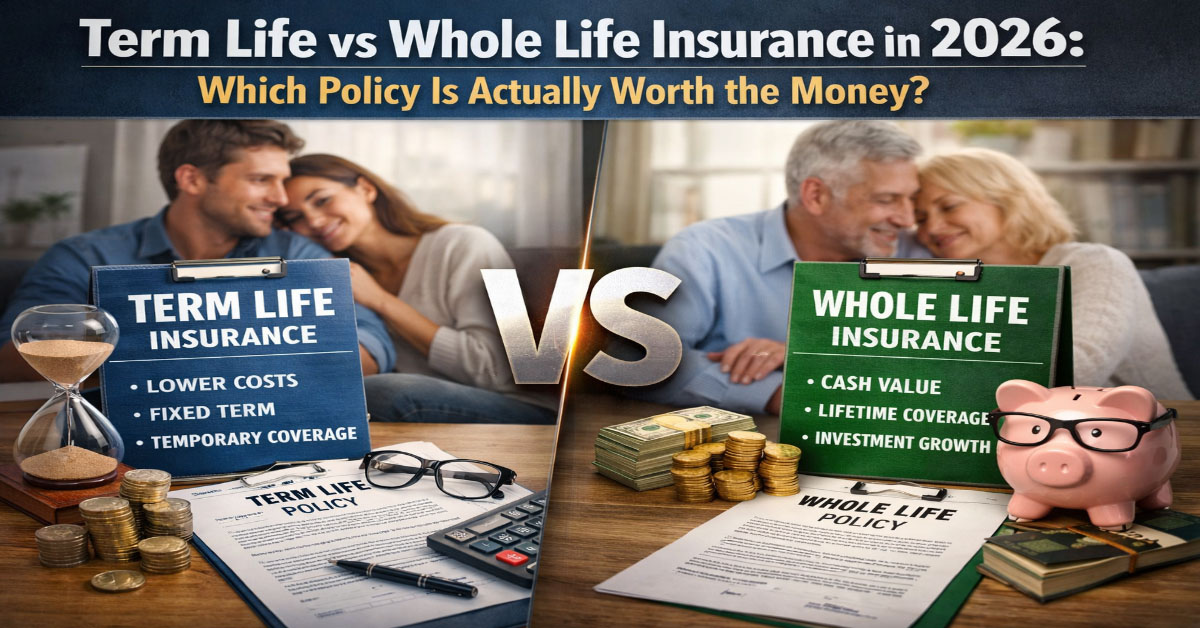

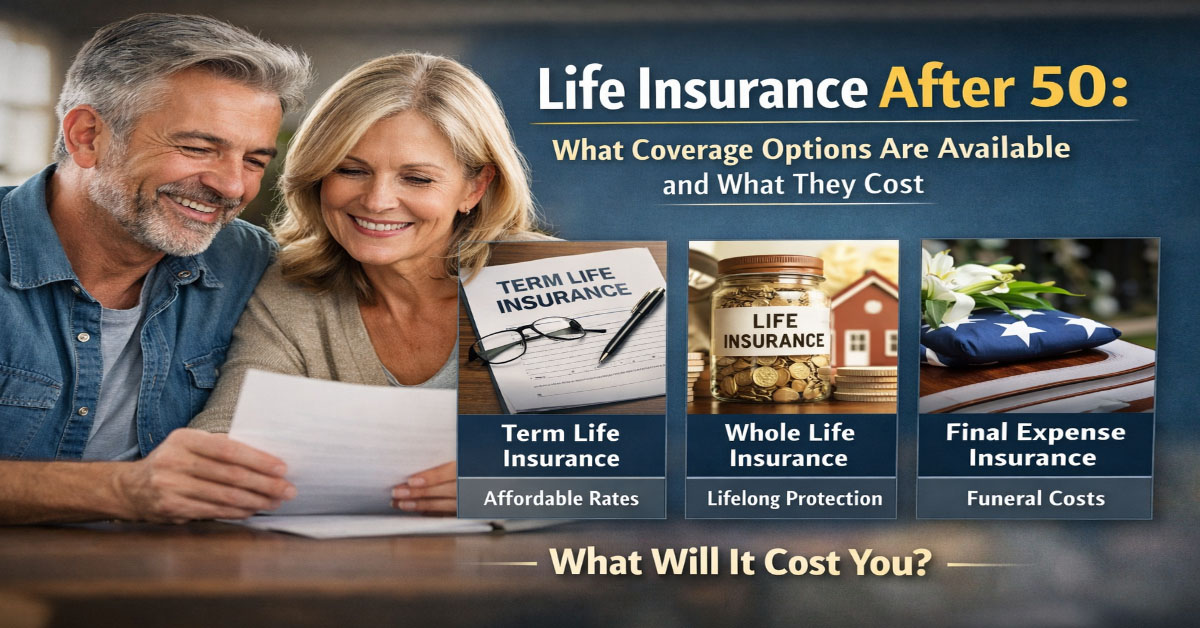

The two most common types are term life and permanent life. Term life provides coverage for a defined period, typically 10, 15, 20, or 30 years, and pays the death benefit only if you die during that term. The premium is fixed for the entire term period. If you outlive the term, the policy expires with no value. Permanent life, including whole life and universal life, provides lifelong coverage and includes a cash value component that accumulates over time. Permanent policies are significantly more expensive than term for the same death benefit amount.

For the majority of people buying life insurance in 2026 for the first time, term life insurance is the appropriate choice. It provides the needed death benefit protection during the years when financial obligations are highest, at a cost that is low enough to make meaningful coverage levels affordable. The specific case for permanent insurance is real but applies to a much narrower set of financial circumstances.

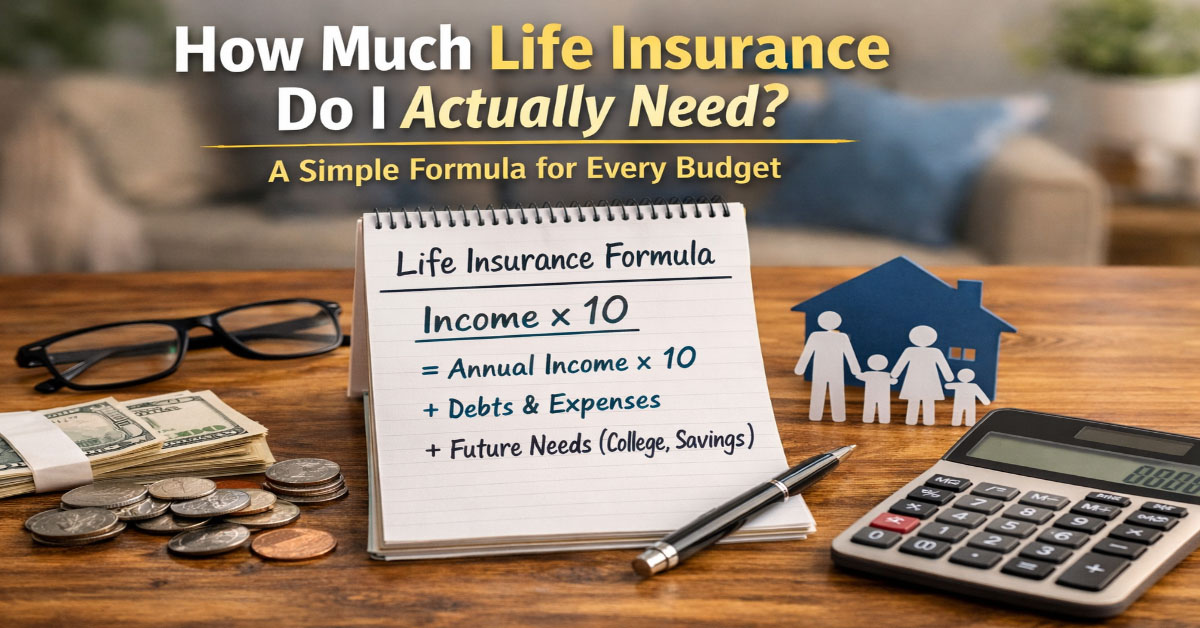

How Much Coverage Do You Actually Need

The most widely used rule of thumb is to carry death benefit coverage equal to 10 to 12 times your annual income. This approximation is reasonable for many households but should be adjusted based on your specific financial circumstances. Key factors that push the number higher include a large mortgage balance, young children who will have significant future education and childcare costs, a non-working spouse who would need to re-enter the workforce and incur retraining or childcare costs, or significant outstanding debts beyond the mortgage.

A more precise approach is the DIME method: add together your total Debt (excluding mortgage), your estimated Income replacement needs for the number of years until your youngest child is financially independent, your Mortgage balance, and your estimated Education costs for all children. The sum of these four figures is your coverage target. For a family with a $350,000 mortgage, two young children, $30,000 in other debt, $80,000 annual income, and 18 years until financial independence, the DIME calculation suggests coverage in the range of $1.5 million to $2 million, a figure that may seem large but costs $50 to $80 per month for a healthy 35-year-old at a 20-year term.

Term vs Whole Life: The Quick Summary

For most people, term life insurance is the right choice. A 20-year, $500,000 term policy for a healthy 35-year-old costs approximately $25 to $35 per month. The same coverage amount in a whole life policy costs $400 to $600 per month. The premium difference of roughly $370 to $565 per month, if invested in a diversified index fund at a 7 percent average return, produces approximately $250,000 to $580,000 in accumulated savings over the 20-year period, usually exceeding the cash value of the whole life policy by a significant margin.

Whole life insurance serves legitimate and specific purposes, including estate liquidity planning, special needs planning for dependents with lifetime financial needs, and situations where someone specifically needs permanent death benefit coverage that cannot expire. For families in the wealth accumulation phase who primarily need to protect against lost income during working years, term life insurance achieves this goal at a fraction of the cost.

The Application and Underwriting Process

Life insurance applications collect information about your health history, family medical history, tobacco and alcohol use, occupation, income, and the amount of coverage you are seeking. For traditional full underwriting, this is followed by a paramedical exam where a trained professional visits your home to collect height, weight, blood pressure, pulse, and a blood and urine sample. Results are reviewed alongside prescription history databases and your driving record to assign you a risk class that determines your premium.

Accelerated underwriting programs, now available from most major carriers for applicants under 60 seeking coverage under $1,000,000 to $2,000,000, use algorithmic review of medical databases, prescription history, and driving records to approve policies without a physical exam. These programs can produce approval decisions in 24 to 72 hours. For healthy applicants with clean records, accelerated underwriting offers the convenience of no exam with competitive pricing.

What Life Insurance Actually Costs in 2026

The persistent overestimation of life insurance costs is one of the primary barriers to purchase. LIMRA survey data consistently shows that Americans estimate term life premiums at three to five times the actual market rate. A healthy 35-year-old male non-smoker can obtain a 20-year, $500,000 term policy for $25 to $35 per month. A 35-year-old female non-smoker pays $20 to $28 per month for the same coverage because women have statistically lower mortality rates. At 45, the same male pays approximately $55 to $75 per month for 20-year, $500,000 term coverage.

Premiums increase with age and health status, which is the most important argument for purchasing coverage sooner rather than later. A policy purchased at 35 locks in that 35-year-old's premium for the entire 20-year term. Waiting until 40 or 45 does not reduce the coverage need but does meaningfully increase the cost. Every year of delay is a year of forgoing coverage at a lower rate than will be available in the future.

How to Get Coverage Quickly

The fastest path to life insurance coverage in 2026 is through a carrier with an accelerated underwriting program that does not require a medical exam for qualifying applicants. Ladder Life, Bestow, and Haven Life are digital-first carriers that have built their entire business model around rapid, exam-free underwriting for eligible applicants. Most major traditional carriers also offer accelerated underwriting pathways for qualifying applications. You can complete the application online, receive approval in as little as one to three business days, and have coverage in force within a week of starting the process.

Common First-Time Buyer Mistakes

The most common mistake is buying too little coverage to keep the premium low. Buying $250,000 in coverage when your household's actual financial need is $1,000,000 provides inadequate protection at a premium that is only marginally lower than adequate coverage would cost. Get the right amount of coverage first, then optimize the term length and other parameters. The premium difference between $500,000 and $1,000,000 in term coverage for a healthy 35-year-old is typically $15 to $25 per month, a small increment for doubling the protection provided.

The second most common mistake is delaying the purchase. Every year of delay is a year without coverage and a year closer to the age at which premiums increase meaningfully. People who consistently defer the purchase decision frequently experience a health change that affects their underwriting class or insurability before they actually buy. The decision to purchase is the hardest step; completing it sooner produces better outcomes at lower long-term cost.

The Life Insurance Application and Underwriting Process

Understanding what happens between submitting a life insurance application and receiving your policy approval helps you prepare effectively, avoid surprises, and set accurate expectations for the timeline and outcome. The underwriting process for term life insurance has become significantly more streamlined in recent years, with many carriers now offering accelerated underwriting that can approve a policy in days rather than weeks for qualifying applicants.

The application collects information about your health history, family medical history, tobacco and alcohol use, occupation, income, aviation or hazardous activity participation, and the amount and purpose of coverage you are seeking. For traditional underwriting, this is followed by a paramedical exam: a trained medical professional visits your home or office to collect height, weight, blood pressure, pulse, and a blood and urine sample. Results are reviewed by the insurer's underwriting team along with prescription history from database sources and your driving record.

Based on underwriting results, you are assigned to a risk class: preferred plus, preferred, standard plus, standard, or substandard table ratings for elevated risk profiles. The risk class determines the premium you are offered. If you qualify for a better risk class than your initial estimate, you pay a lower premium than quoted. If underwriting reveals a health condition that increases your risk, you may be offered coverage at a higher premium than initially estimated or declined for coverage in rare cases.

Accelerated underwriting programs, now available from most major carriers for applicants under 60 seeking coverage under $1,000,000 to $2,000,000, use algorithmic review of medical database records, prescription history, and driving record to approve policies without a physical exam. These programs can produce approval decisions in as little as 24 to 72 hours. For healthy applicants with clean records, accelerated underwriting offers the convenience of no exam with competitive pricing. Applicants with health conditions or complex profiles may receive better risk class assignments through traditional full underwriting that includes a physical exam and more comprehensive medical history review.

Naming Beneficiaries: The Most Important Decision After Buying Coverage

The beneficiary designation on a life insurance policy determines who receives the death benefit when the insured dies. This designation supersedes any instructions in a will. It is one of the most consequential financial decisions a policyholder makes, and yet it is also one of the most commonly overlooked after the initial policy purchase.

Every life insurance policy should have a primary beneficiary and at least one contingent beneficiary designated. The primary beneficiary receives the death benefit if they are alive at the time of the claim. The contingent beneficiary receives the benefit if the primary beneficiary has predeceased the insured. Without a contingent beneficiary designation, the benefit would pass to the insured's estate if the primary predeceases them, which can trigger probate, creditor claims, and estate taxes that undermine the purpose of the coverage.

Review your beneficiary designations after every major life change: marriage, divorce, birth of a child, death of a named beneficiary, or significant change in family financial circumstances. Outdated beneficiary designations that still name an ex-spouse are an unfortunately common and easily preventable error that causes significant distress to surviving family members. Contact your insurer directly to update beneficiary information rather than relying on a will or other estate document, since the beneficiary designation on the policy itself is the legally controlling document.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.