Artificial intelligence has transformed the life insurance application process more dramatically in the past three years than any other period in the industry's history. What used to require multiple in-person agent meetings, a paramedical exam involving blood draws and medical history interviews, and three to six weeks of underwriting review can now, for qualifying applicants, be completed entirely online in 20 to 30 minutes with an algorithmic approval decision in 24 to 72 hours. AI tools have also transformed how consumers compare policies, estimate coverage needs, and manage existing coverage throughout the policy's life.

This guide reviews the landscape of AI-powered life insurance tools in 2026: what they do well, where they have real limitations, which categories of buyers benefit most, which categories should proceed with caution, and how to use these tools most effectively to get the right coverage at the lowest available rate.

In This Article

- Categories of AI Life Insurance Tools

- AI Underwriting: How Accelerated Approval Works

- Best Candidates for AI-Driven Underwriting

- AI Comparison and Recommendation Tools

- Top Digital-First Carriers in 2026

- Where AI Tools Fall Short

- When Traditional Underwriting Still Wins

- Data Privacy Considerations

- Where AI in Life Insurance Is Heading

Categories of AI Life Insurance Tools

AI tools in the life insurance space fall into four main functional categories, each serving different stages of the coverage decision and management process. Understanding what each category does helps you deploy the right tool for the right purpose.

The first category is accelerated underwriting engines, which use AI and machine learning to analyze medical database records, prescription history, driving records, and in some cases wearable device data to make underwriting decisions algorithmically without requiring a human underwriter to review each application or a physical medical exam. These systems represent the most significant operational transformation in life insurance and are the primary reason application processes have shortened from weeks to days.

The second category is AI comparison and recommendation tools, which gather information about your coverage needs, health profile, and financial situation and provide personalized policy comparisons across multiple carriers. These tools range from simple quote aggregators that present premium comparisons to sophisticated needs-analysis engines that recommend specific coverage types, amounts, and term lengths based on your stated circumstances.

The third category is AI-powered chatbot and virtual agent tools that guide applicants through the application process, answer coverage questions, and provide real-time guidance. These systems replace or supplement traditional agent interactions for straightforward coverage situations. The fourth category is post-purchase AI tools that help policyholders manage their coverage, understand policy terms, track beneficiary designations, and identify when coverage review is warranted based on life changes.

AI Underwriting: How Accelerated Approval Works

Traditional life insurance underwriting involved a paramedical exam, laboratory analysis of blood and urine samples, physician statement requests from your doctors, prescription database lookups, and human underwriter review of all gathered information. This process took three to six weeks and was a significant friction point that caused many would-be buyers to abandon the process.

Accelerated underwriting engines replace much of this process with algorithmic analysis of existing data sources. The primary data sources accessed include MIB Group medical records, prescription drug history from major pharmacy databases, DMV driving records, public records, and in some programs, consumer financial data and behavioral analytics. The AI system synthesizes these data sources against actuarial risk models trained on millions of prior applications and their associated mortality outcomes, producing a risk classification decision in minutes rather than weeks.

For applicants who are genuinely healthy, the data in these source systems is accurate, and the coverage amount is within the program's eligibility limits, accelerated underwriting produces fully binding policy offers with the same pricing available through traditional underwriting but without the exam and waiting period. Most major carriers offer accelerated underwriting for coverage amounts up to $1,000,000 to $2,000,000 for applicants under age 60.

Best Candidates for AI-Driven Underwriting

The ideal AI underwriting candidate is a healthy adult under 55 with no significant medical history, seeking coverage amounts under $1,500,000, with a clean driving record, no tobacco use, and no high-risk occupational or recreational activities. This profile describes a large proportion of first-time life insurance buyers, which is why accelerated underwriting has been transformative for the industry's ability to reach and serve this market segment.

Young adults in their 20s and early 30s who have never needed significant medical care and have minimal prescription history are particularly well-served by accelerated underwriting. Their sparse medical records present less complexity for the AI system to evaluate, and their clean profiles almost universally trigger straightforward approvals at preferred or preferred-plus rate classes within hours of application.

Parents in their 30s and early 40s who are buying coverage for the first time after a life event like a new child or home purchase are the largest single market segment served by these tools. The combination of a clear coverage motivation, reasonable health for their age cohort, and the convenience of a process that fits around a busy family schedule has driven strong adoption in this demographic.

AI Comparison and Recommendation Tools

AI-powered comparison tools have made life insurance shopping more transparent and less agent-dependent than at any point in the product's history. Platforms like Policygenius, SelectQuote, and numerous direct carrier tools use intake questionnaires to gather health and financial information and produce personalized premium comparisons across multiple carriers within minutes. The best of these tools go beyond simple price comparison to provide recommendations about coverage type, amount, and term length based on the user's stated circumstances.

The quality of AI recommendation tools varies considerably. Tools that ask detailed questions about household income, outstanding debt, mortgage balance, number and ages of children, existing coverage, and savings level produce more meaningful coverage recommendations than tools that simply ask for age and income and multiply by a fixed factor. Taking extra time to provide accurate and complete information to these tools produces more useful outputs that are worth the investment of a few additional minutes.

One important caveat about AI comparison tools: they are often owned by or affiliated with specific carriers or broker networks that may not have agreements with every insurer in the market. A comparison tool that shows you quotes from five carriers may be missing the sixth carrier that would offer you the most competitive rate for your specific health profile. Using multiple comparison tools and checking directly with carriers that are known to be competitive for your demographic, including USAA for eligible military members, can surface options that no single comparison platform surfaces.

Top Digital-First Carriers in 2026

Several carriers have built their business models entirely around digital-first, AI-powered application and underwriting processes, producing the fastest and most frictionless application experiences available in 2026.

Ladder Life is a digital-first carrier that allows policyholders to adjust their coverage up or down as their needs change, which is a genuinely innovative feature that no traditional carrier offers in the same way. Bestow processes applications entirely online with no medical exam required for qualifying applicants and has been recognized for its transparent pricing and straightforward user experience. Haven Life, backed by MassMutual, combines digital-first application convenience with the financial strength and claims reliability of one of the oldest insurance companies in the country, which addresses a concern some consumers have about newer digital carriers. Fabric by Gerber Life focuses specifically on young families and offers a simplified online experience designed for first-time buyers who have not previously navigated the traditional life insurance process.

Traditional carriers including Protective, Banner Life, Principal, and Pacific Life all offer accelerated underwriting programs alongside their traditional underwriting options, combining competitive pricing with the financial stability track record of established companies. For coverage amounts above the typical accelerated underwriting limit, these carriers often provide the most competitive rates through traditional full underwriting.

Where AI Tools Fall Short

AI underwriting tools perform well for the specific profiles they were trained on but have real limitations for applicants outside that profile. Complex medical histories involving multiple conditions, prior hospitalizations, surgical history, or mental health treatment are areas where algorithmic systems frequently require escalation to human underwriters or produce conservative risk classifications that overstate the actual mortality risk for that individual. A human underwriter reviewing the same file with judgment and context can sometimes assign a more favorable risk class than the algorithmic decision-tree would produce.

Lifestyle factors that increase risk, including certain high-risk occupations, aviation activity, scuba diving, rock climbing, and motorsports, are sometimes handled more sophisticatedly by experienced human underwriters than by AI systems that apply fixed rate-ups without nuance about the specific nature and frequency of the risky activity.

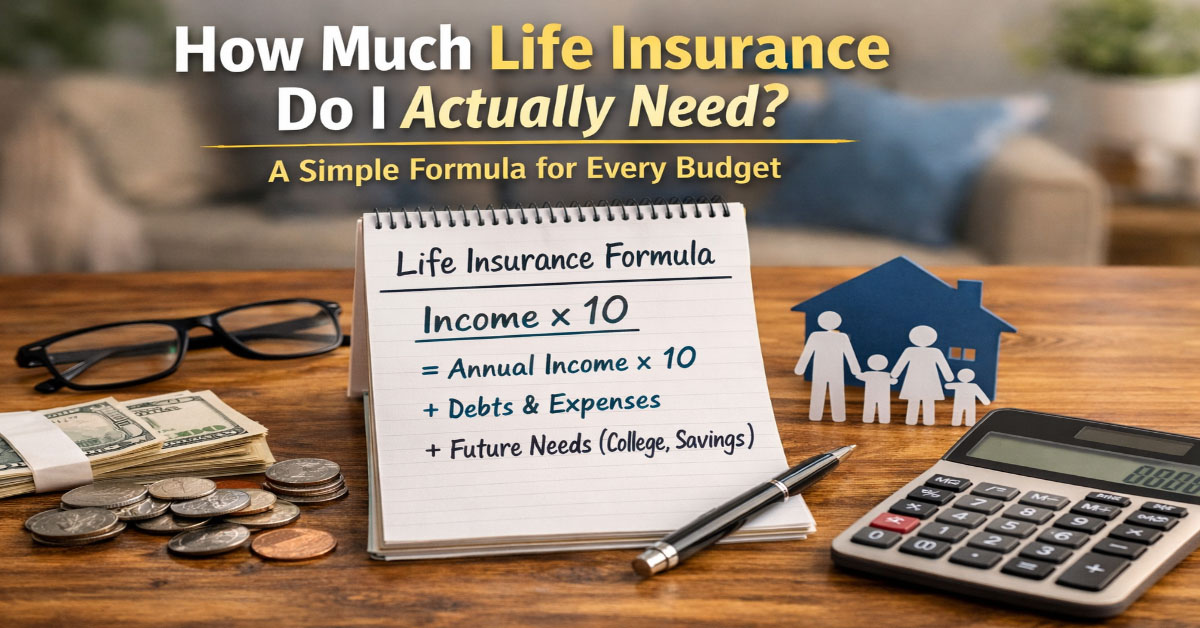

Coverage needs analysis is another area where AI tools have clear limitations. A sophisticated AI comparison tool that produces a coverage amount recommendation based on a questionnaire is not a substitute for a comprehensive financial planning conversation that considers your complete balance sheet, debt structure, estate plan, business interests, and family-specific circumstances. The algorithmic recommendation is a useful starting point but should be validated against a more thorough analysis for complex situations.

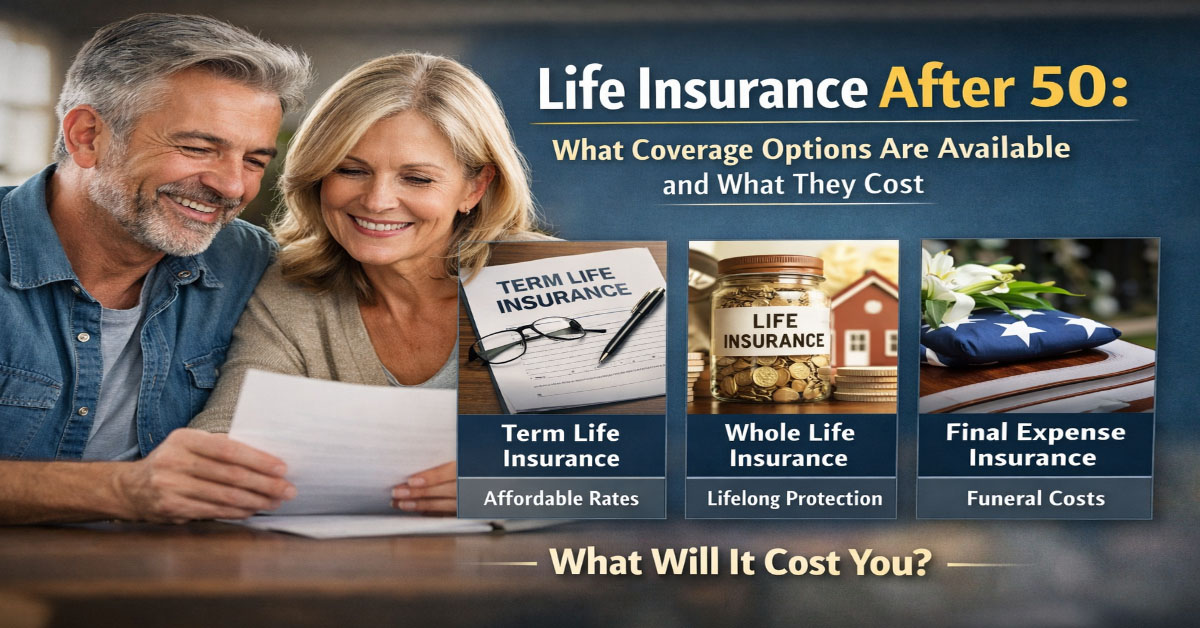

When Traditional Underwriting Still Wins

For applicants with health histories, traditional full underwriting including a paramedical exam remains the better path in several specific situations. If you have a condition that is well-controlled and stable, a physician's documentation of your management and outcomes can tell a more favorable story than prescription history and database records alone, sometimes producing a better risk class through traditional underwriting than an algorithmic decision based on incomplete data.

If you are applying for coverage amounts above $2,000,000, most accelerated programs reach their limits and full underwriting is required regardless of health status. For high-coverage amounts, the time investment in full underwriting is justified by the coverage level being secured and the importance of getting the most accurate risk classification possible. Family history of significant hereditary conditions, while not disqualifying for coverage, is best addressed through a conversation with a knowledgeable underwriter rather than through an algorithm that applies standard rate-ups without the opportunity for context and documentation to improve the assessment.

Data Privacy Considerations

AI-powered life insurance underwriting relies on extensive data collection about your health, prescriptions, finances, and behavior. Understanding what data is being accessed and how it is used is important before completing an application. The MIB Group, prescription history databases, and DMV records are the primary external data sources, and most carriers are required to disclose that they access these sources. Federal law provides some protections around how this data can be used in underwriting decisions, and insurers that use credit or consumer data for underwriting purposes are subject to Fair Credit Reporting Act requirements including adverse action notification if data contributed to an unfavorable decision.

Wearable device data, including step counts, heart rate data, and sleep metrics from devices like Fitbit, Apple Watch, and Garmin, is being explored by some carriers as a voluntary data-sharing program that can improve risk classification for healthy, active applicants. These programs are currently voluntary and should be evaluated based on your specific data profile before opting in. An applicant with excellent activity data whose metrics strongly support a favorable health profile may benefit from participation. An applicant whose metrics are less favorable is better served by the standard underwriting process that does not access this data.

Where AI in Life Insurance Is Heading

The trajectory of AI in life insurance over the next five years points toward further acceleration and personalization. Real-time underwriting that produces policy offers within seconds of application completion is technically feasible and will likely become the standard for qualified applicants rather than the exception. Continuous underwriting models that adjust pricing or coverage terms based on ongoing health and behavioral data, with policyholder consent, are in early development at several carriers. The elimination of medical exams for coverage amounts well above current accelerated underwriting limits is a likely development as AI systems accumulate more training data and demonstrate actuarial equivalence with exam-based underwriting for increasingly complex applicant profiles.

The human life insurance agent will remain relevant in this environment for complex situations, high coverage amounts, business insurance planning, and clients who value the relationship dimension of working with a trusted advisor. But for the majority of straightforward individual life insurance needs, the AI-powered direct model will continue capturing an increasing share of the market as its cost, speed, and convenience advantages compound over time.

The Life Insurance Application and Underwriting Process

Understanding what happens between submitting a life insurance application and receiving your policy approval helps you prepare effectively, avoid surprises, and set accurate expectations for the timeline and outcome. The underwriting process for term life insurance has become significantly more streamlined in recent years, with many carriers now offering accelerated underwriting that can approve a policy in days rather than weeks for qualifying applicants.

The application collects information about your health history, family medical history, tobacco and alcohol use, occupation, income, aviation or hazardous activity participation, and the amount and purpose of coverage you are seeking. For traditional underwriting, this is followed by a paramedical exam: a trained medical professional visits your home or office to collect height, weight, blood pressure, pulse, and a blood and urine sample. Results are reviewed by the insurer's underwriting team along with prescription history from database sources and your driving record.

Based on underwriting results, you are assigned to a risk class: preferred plus, preferred, standard plus, standard, or substandard table ratings for elevated risk profiles. The risk class determines the premium you are offered. If you qualify for a better risk class than your initial estimate, you pay a lower premium than quoted. If underwriting reveals a health condition that increases your risk, you may be offered coverage at a higher premium than initially estimated or declined for coverage in rare cases.

Accelerated underwriting programs, now available from most major carriers for applicants under 60 seeking coverage under $1,000,000 to $2,000,000, use algorithmic review of medical database records, prescription history, and driving record to approve policies without a physical exam. These programs can produce approval decisions in as little as 24 to 72 hours. For healthy applicants with clean records, accelerated underwriting offers the convenience of no exam with competitive pricing. Applicants with health conditions or complex profiles may receive better risk class assignments through traditional full underwriting that includes a physical exam and more comprehensive medical history review.

Naming Beneficiaries: The Most Important Decision After Buying Coverage

The beneficiary designation on a life insurance policy determines who receives the death benefit when the insured dies. This designation supersedes any instructions in a will. It is one of the most consequential financial decisions a policyholder makes, and yet it is also one of the most commonly overlooked after the initial policy purchase.

Every life insurance policy should have a primary beneficiary and at least one contingent beneficiary designated. The primary beneficiary receives the death benefit if they are alive at the time of the claim. The contingent beneficiary receives the benefit if the primary beneficiary has predeceased the insured. Without a contingent beneficiary designation, the benefit would pass to the insured's estate if the primary predeceases them, which can trigger probate, creditor claims, and estate taxes that undermine the purpose of the coverage.

Review your beneficiary designations after every major life change: marriage, divorce, birth of a child, death of a named beneficiary, or significant change in family financial circumstances. Outdated beneficiary designations that still name an ex-spouse are an unfortunately common and easily preventable error that causes significant distress to surviving family members. Contact your insurer directly to update beneficiary information rather than relying on a will or other estate document, since the beneficiary designation on the policy itself is the legally controlling document.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.