Life insurance after age 50 occupies a complicated position in financial planning. For people who have carried life insurance throughout their 30s and 40s and maintained strong health, the question at 50 is often whether to renew, replace, or reduce coverage as the original protection needs have evolved. For people who are buying life insurance for the first time in their 50s, the question is whether coverage is still obtainable, what it costs, and whether the premium justifies the protection at this stage of life.

This guide addresses both situations with honest, current information about what is available in 2026, what it realistically costs, how underwriting works for this age group, and the specific situations where buying or maintaining life insurance after 50 genuinely makes sense financially.

In This Article

- Who Still Needs Life Insurance After 50

- Life Insurance Options Available After 50

- What Life Insurance Costs After 50 in 2026

- How Health Affects Premiums and Insurability at 50 Plus

- Renewing or Replacing an Expiring Term Policy

- When to Reduce Coverage Rather Than Replace It

- No-Exam Options for the 50-Plus Market

- Final Expense Insurance: What It Is and When It Makes Sense

- Permanent Insurance After 50

- Making the Decision for Your Situation

Who Still Needs Life Insurance After 50

The need for life insurance after 50 depends heavily on your specific financial circumstances, not your age alone. Several situations create a genuine ongoing need for coverage at this life stage.

Ongoing financial dependents remain the clearest indicator of continued coverage need. If you have minor children from a later marriage or second family, dependent adult children with disabilities, or aging parents who depend on your financial support, the income replacement rationale for life insurance continues to apply even after 50. The coverage amount may be lower than what a 35-year-old with the same obligations would carry because your remaining working years are fewer and your expected savings accumulation is larger, but the need is real.

A working spouse who would suffer significant financial hardship without your income is another ongoing need indicator. If your combined retirement savings are not yet at a level that would sustain your spouse's lifestyle independently, the income protection rationale continues. A spouse who is 10 or more years younger and has not yet built their own retirement security is a particularly clear case for maintaining coverage.

Significant outstanding mortgage debt on a home that your spouse could not service alone on their income, particularly in a market where selling quickly at a fair price might be difficult, supports maintaining coverage sized to the mortgage balance. Business ownership with an active buy-sell agreement, estate liquidity needs for an estate that would face tax obligations, and large outstanding co-signed debts are additional situations where coverage after 50 is genuinely warranted rather than merely optional.

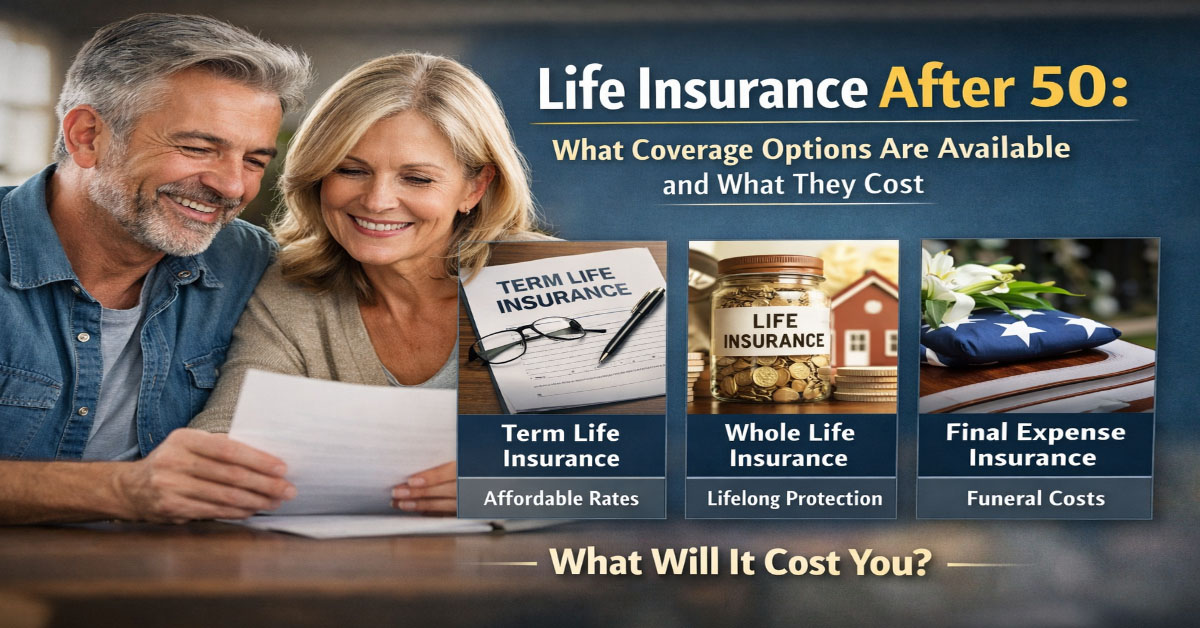

Life Insurance Options Available After 50

The life insurance options available at 50 through 65 include term life insurance in shorter durations, permanent life insurance in several forms, guaranteed issue life insurance for people who cannot qualify medically for standard coverage, and simplified issue policies that use health questionnaires rather than full medical underwriting. The availability of each option and its pricing depend significantly on your specific health profile and the coverage amount you need.

Term life insurance remains available after 50 but typically in shorter maximum term lengths than at younger ages. At 52, a 20-year term policy would provide coverage to age 72, which is within the range many carriers are willing to write. A 30-year term at 52 would run to age 82, a longer duration that fewer carriers offer and that commands significantly higher premiums. Most major carriers offer 10 and 15-year terms at attractive pricing for healthy applicants in their 50s, and some offer 20-year terms for applicants with excellent health profiles.

What Life Insurance Costs After 50 in 2026

Premiums increase meaningfully with age, and the jump from the 40s to the 50s is significant. Understanding realistic 2026 premium ranges for different coverage amounts and health profiles helps set appropriate expectations before you begin the application process.

Approximate Term Life Premiums After 50: 2026

These ranges represent healthy applicants who qualify for standard or better underwriting classes. Applicants with common age-related conditions including controlled hypertension, controlled Type 2 diabetes, elevated cholesterol, or BMI in the overweight range will pay higher premiums in the table-rated or substandard tier, sometimes 25 to 100 percent above standard rates depending on the specific condition, its severity, and how well it is controlled.

How Health Affects Insurability and Premiums at 50 Plus

Health becomes increasingly important to the underwriting decision as buyers age because the statistical mortality risk at any given health status level is higher at 55 than at 35. Conditions that would result in a standard risk class for a healthy 35-year-old might result in a table-rated substandard class for a 57-year-old with the same condition, because the mortality impact of the condition compounds with the baseline mortality risk that increases with age.

However, well-controlled conditions with strong documentation of management are underwritten more favorably than uncontrolled or recently diagnosed conditions. A 54-year-old with Type 2 diabetes well-controlled on a single medication with an A1C consistently below 7.0 and no complications typically qualifies for coverage, perhaps at a table rating, while a 54-year-old with the same diagnosis but poor control or recent complications may face difficulty obtaining standard coverage. Working with an independent broker who understands the underwriting criteria of multiple carriers can be particularly valuable for applicants with health histories, because different carriers have different underwriting philosophies for specific conditions and the pricing difference between the most and least favorable carrier for a given condition can be very significant.

Renewing or Replacing an Expiring Term Policy

Many people in their 50s are facing the expiration of a 20 or 30-year term policy they bought in their 30s or earlier. The options at expiration are allowing the policy to lapse and going without coverage, renewing the term at the annual renewable term premium which will be very high, converting the term to a permanent policy at current attained-age rates if the conversion option is still available, or replacing the policy with a new term or permanent policy subject to current health-based underwriting.

The conversion option is worth examining carefully before the deadline passes. Most term policies include a conversion right that allows conversion to a permanent policy without new medical underwriting. The permanent policy is priced at attained-age rates without reference to your current health, which means someone whose health has declined since the original term purchase can convert to guaranteed permanent coverage at rates that would not be available through new underwriting. The conversion deadline is specified in the policy, often age 65 or a defined number of years before policy expiration, and missing it eliminates the option permanently.

When to Reduce Coverage Rather Than Replace It

For people whose coverage needs have genuinely decreased, reducing coverage rather than replacing the full amount is often the financially rational approach. If your mortgage is nearly paid off, your children are financially independent, your retirement savings have grown to a level that could support your spouse independently, and your primary remaining coverage rationale is modest income supplementation for a few remaining working years, a smaller policy at lower cost may serve your actual needs better than a full income-multiple policy at high post-50 premiums.

The coverage reduction decision should be based on a current analysis of your household's actual financial vulnerability rather than on the amount of coverage you carried when you were 38 with young children and a large mortgage. Your financial situation at 54 is different, and the coverage appropriate for that situation may be meaningfully different from what was appropriate at 38.

No-Exam Options for the 50-Plus Market

Accelerated underwriting programs extend to applicants in their 50s with varying coverage limits. Many carriers will offer accelerated, no-exam underwriting for applicants up to age 60 seeking coverage up to $500,000 to $1,000,000 who meet general health eligibility criteria. For applicants in their early to mid-50s with genuinely excellent health, the accelerated process can produce competitive approvals without the exam burden at reasonably attractive rates.

Simplified issue policies, which use a health questionnaire rather than full medical underwriting or a paramedical exam, are available from multiple carriers for the 50-plus market at coverage amounts typically ranging from $25,000 to $400,000. These policies are more expensive per dollar of coverage than fully underwritten policies for applicants who can qualify for standard rates, but they provide access to coverage for people whose health history makes full underwriting uncertain or undesirable.

Final Expense Insurance: What It Is and When It Makes Sense

Final expense insurance, also called burial insurance or funeral insurance, is a small whole life policy designed to cover end-of-life costs including funeral and burial expenses, which currently average $8,000 to $12,000 nationally. These policies are typically issued with face amounts of $5,000 to $25,000 and are available to applicants between approximately 50 and 85 with minimal medical underwriting.

Final expense insurance serves a legitimate purpose for people who have no other life insurance, have no savings set aside for end-of-life expenses, and do not want to leave their family with an immediate large financial burden at the time of death. It is not a replacement for income protection coverage but can provide meaningful peace of mind for people whose primary insurance need is specifically end-of-life expense coverage rather than income replacement.

The premiums for final expense policies are relatively high on a cost-per-dollar-of-coverage basis compared to fully underwritten term life insurance because they are accessible to older and less-healthy applicants who could not qualify for standard coverage. Applicants who can qualify for standard term coverage are almost always better served by a traditional underwritten policy at lower per-dollar cost.

Permanent Insurance After 50

For people with genuine permanent insurance needs including estate liquidity, buy-sell business agreements, or special needs dependents, permanent insurance purchased in the 50s can still serve its purpose effectively. The premiums are substantially higher than for the same coverage purchased at 35 or 40, which is why the decision to buy permanent coverage should be validated against a genuine, specific permanent need rather than a general desire for lifelong coverage.

Guaranteed universal life insurance, sometimes called GUL, is often the most cost-effective form of permanent coverage for people in their 50s who need a death benefit guarantee rather than cash value accumulation. GUL policies provide permanent death benefit coverage at premiums lower than traditional whole life because they are designed primarily to maintain the death benefit to a specified age like 90 or 100, with minimal cash value accumulation. For estate liquidity and buy-sell purposes, the death benefit guarantee is the valuable feature; the cash value accumulation of whole life is not necessary for these use cases and the premium savings of GUL over whole life can be substantial.

Making the Decision for Your Situation

The decision about life insurance after 50 should begin with an honest assessment of your current household's financial vulnerability in the event of your death. If your surviving spouse could maintain their lifestyle and financial security without your income or death benefit payment, coverage is optional regardless of premium levels or carrier availability. If your surviving spouse, dependents, or business partners would face meaningful financial hardship, coverage remains important even at the higher premiums that reflect your age and risk profile.

Get quotes before making any assumptions about affordability. Many people in their 50s are pleasantly surprised by the premiums available to them, particularly those in genuinely good health. A healthy 54-year-old with excellent bloodwork, no tobacco use, and well-managed numbers can often qualify for standard or preferred risk classes at premiums that are high compared to their 35-year-old self but manageable as a monthly expense relative to the protection provided.

The Life Insurance Application and Underwriting Process

Understanding what happens between submitting a life insurance application and receiving your policy approval helps you prepare effectively, avoid surprises, and set accurate expectations for the timeline and outcome. The underwriting process for term life insurance has become significantly more streamlined in recent years, with many carriers now offering accelerated underwriting that can approve a policy in days rather than weeks for qualifying applicants.

The application collects information about your health history, family medical history, tobacco and alcohol use, occupation, income, aviation or hazardous activity participation, and the amount and purpose of coverage you are seeking. For traditional underwriting, this is followed by a paramedical exam: a trained medical professional visits your home or office to collect height, weight, blood pressure, pulse, and a blood and urine sample. Results are reviewed by the insurer's underwriting team along with prescription history from database sources and your driving record.

Based on underwriting results, you are assigned to a risk class: preferred plus, preferred, standard plus, standard, or substandard table ratings for elevated risk profiles. The risk class determines the premium you are offered. If you qualify for a better risk class than your initial estimate, you pay a lower premium than quoted. If underwriting reveals a health condition that increases your risk, you may be offered coverage at a higher premium than initially estimated or declined for coverage in rare cases.

Accelerated underwriting programs, now available from most major carriers for applicants under 60 seeking coverage under $1,000,000 to $2,000,000, use algorithmic review of medical database records, prescription history, and driving record to approve policies without a physical exam. These programs can produce approval decisions in as little as 24 to 72 hours. For healthy applicants with clean records, accelerated underwriting offers the convenience of no exam with competitive pricing. Applicants with health conditions or complex profiles may receive better risk class assignments through traditional full underwriting that includes a physical exam and more comprehensive medical history review.

Naming Beneficiaries: The Most Important Decision After Buying Coverage

The beneficiary designation on a life insurance policy determines who receives the death benefit when the insured dies. This designation supersedes any instructions in a will. It is one of the most consequential financial decisions a policyholder makes, and yet it is also one of the most commonly overlooked after the initial policy purchase.

Every life insurance policy should have a primary beneficiary and at least one contingent beneficiary designated. The primary beneficiary receives the death benefit if they are alive at the time of the claim. The contingent beneficiary receives the benefit if the primary beneficiary has predeceased the insured. Without a contingent beneficiary designation, the benefit would pass to the insured's estate if the primary predeceases them, which can trigger probate, creditor claims, and estate taxes that undermine the purpose of the coverage.

Review your beneficiary designations after every major life change: marriage, divorce, birth of a child, death of a named beneficiary, or significant change in family financial circumstances. Outdated beneficiary designations that still name an ex-spouse are an unfortunately common and easily preventable error that causes significant distress to surviving family members. Contact your insurer directly to update beneficiary information rather than relying on a will or other estate document, since the beneficiary designation on the policy itself is the legally controlling document.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.