The cyberthreat landscape facing businesses in 2026 has been fundamentally transformed by artificial intelligence. Attackers deploy AI-generated voice and video to impersonate executives and clients in real time. They use large language models to craft phishing emails indistinguishable from legitimate communications. They automate the reconnaissance and exploitation phases of attacks, dramatically reducing the cost and time required to compromise business systems. These developments have challenged the insurance industry to adapt coverages designed for an older threat model to a faster-moving, more sophisticated risk environment where the attack surfaces keep expanding.

This guide explains the specific AI-driven threats that businesses face in 2026, how standard cyber insurance policies do and do not respond to these new attack types, the coverage gaps that require specific attention, and how forward-looking businesses are adapting both their risk management practices and their insurance programs to address the evolved threat landscape.

In This Article

- Deepfake Fraud: The New Business Threat

- AI-Powered Phishing and Social Engineering

- Ransomware Evolution in 2026

- How Cyber Insurance Responds to AI Threats

- Coverage Gaps and Exclusions

- Social Engineering and Funds Transfer Fraud Coverage

- How Insurers Are Adapting Underwriting

- Controls That Reduce Both Risk and Premium

- The Future of Business Cyber Insurance

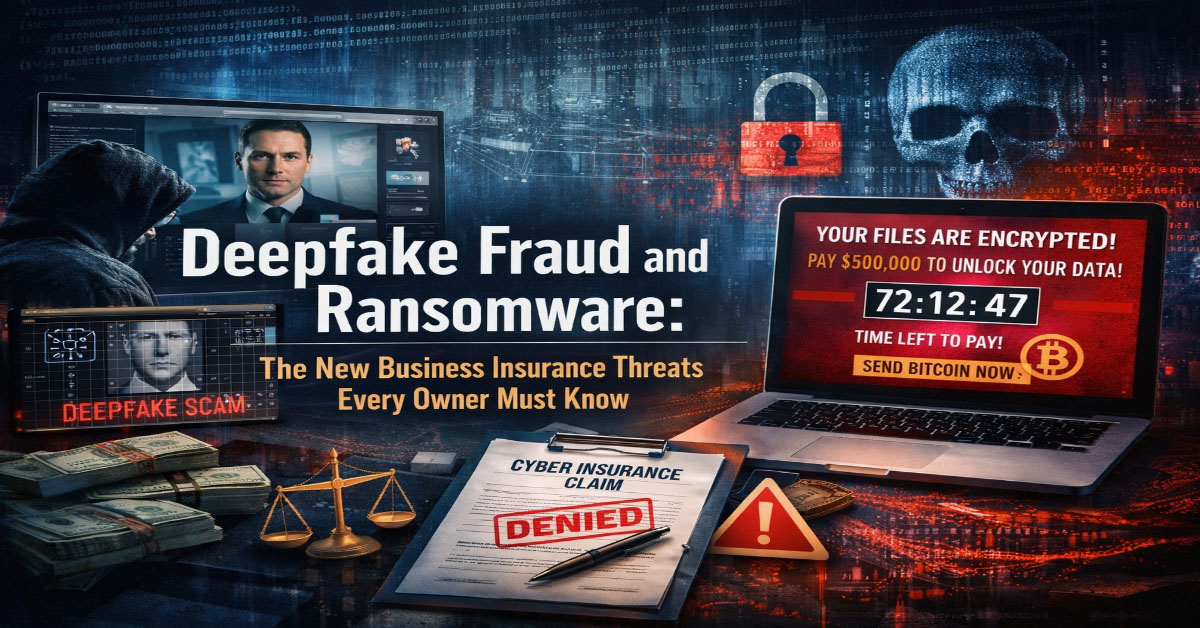

Deepfake Fraud: The Emerging Business Threat in 2026

Deepfake technology that generates highly convincing synthetic audio and video of real individuals has moved from a theoretical concern into an active business fraud vector. The most documented incident type involves attackers using AI-generated voice cloning to impersonate senior executives in phone calls to finance staff, instructing them to make urgent wire transfers to attacker-controlled accounts. These voice cloning attacks are effective because they present the convincing vocal characteristics and communication style of the person being impersonated, bypassing the skepticism that an email from an unknown source would trigger.

Video deepfake incidents have progressed from still-image manipulation to real-time video call impersonation in documented 2025 and 2026 incidents. A finance employee conducting what they believe is a video verification call with their CFO approving a large transaction may be interacting with an AI-generated video overlay of their actual CFO's face applied to an attacker's video stream. While technically demanding, these attacks are no longer exclusively available to well-resourced nation-state actors; commercial deepfake tools have become accessible to sophisticated criminal organizations with the motivation to invest in high-return fraud techniques.

Financial losses from deepfake-enabled fraud can be substantial. Documented cases include wire transfers ranging from $25,000 to $35,000,000 transferred based on deepfake executive impersonation. These losses fall into the social engineering or fraudulent instruction category of cyber losses rather than the traditional network intrusion or ransomware category, which means standard cyber policies that do not explicitly include social engineering fraud coverage may not respond to these claims regardless of the total loss amount.

AI-Powered Phishing and Social Engineering

Traditional phishing emails were identifiable by generic messaging, grammatical errors, suspicious links, and impersonal salutations. AI-generated phishing emails in 2026 are personalized, grammatically correct, contextually aware of the recipient's role and relationships, and often reference real recent events or communications that add credibility to the malicious request. Spear phishing has become significantly more scalable as AI tools allow attackers to generate dozens of highly personalized attack emails at the cost and time previously required to write one carefully researched message.

Business email compromise attacks have become more sophisticated as AI assists attackers in analyzing legitimate email chains, understanding organizational relationships, mimicking communication styles, and timing fraudulent requests to coincide with real business processes like vendor payment cycles or periods when key approvers are traveling and harder to reach for verification. The sophistication of these attacks makes employee awareness training more important than ever while simultaneously making that training more difficult to make effective because the attacks are designed to defeat detection by trained, vigilant employees.

Ransomware Evolution in 2026

Ransomware has continued to evolve in sophistication and impact. The dominant model in 2026 is ransomware as a service, where criminal organizations develop and maintain ransomware platforms that they license to affiliate attackers who conduct the actual intrusions and pay a revenue share to the platform operators. This model has dramatically expanded the number of active threat actors by separating the technical development work from the attack execution work, lowering the barrier to entry for new criminal actors who can access sophisticated attack tools without developing them independently.

The double extortion model combining file encryption with data exfiltration and publication threats has become the standard approach for sophisticated ransomware groups. This creates two distinct insurance coverage needs: business interruption coverage for the operational downtime while systems are restored or rebuilt, and data breach notification and liability coverage for the exfiltrated data if it contains personal information about customers, employees, or other protected parties. Full incident response, forensic investigation, and system rebuild costs following a serious ransomware attack frequently exceed the ransom payment amount itself, reaching $500,000 to $2,000,000 or more for businesses with substantial operations and data environments.

How Cyber Insurance Responds to AI-Driven Threats

Modern cyber insurance policies respond to the consequences of a covered cyber incident regardless of the specific technical mechanism used to cause the incident, provided the incident falls within the policy's coverage definitions. A ransomware attack that encrypts systems and causes business interruption will be covered under a comprehensive cyber policy whether the ransomware was delivered through a phishing email, a credential stuffing attack, or an AI-assisted targeted intrusion, assuming no specific exclusion applies.

The more nuanced question is whether specific emerging threats, particularly deepfake-enabled social engineering fraud and AI-generated phishing that results in direct financial transfer rather than system compromise, fall within the coverage definitions of a given policy. A deepfake voice call that causes an employee to wire $500,000 to a fraudulent account is not a network security incident in the traditional sense. There was no unauthorized access to your computer systems. The attacker never penetrated your network. Yet the financial loss is real and substantial. Whether this loss is covered depends entirely on whether your policy includes social engineering or fraudulent instruction coverage with an adequate sublimit.

Coverage Gaps to Watch For

The social engineering gap is the most critical coverage gap for businesses facing AI-driven threats in 2026. Many cyber policies either exclude social engineering losses entirely or include them only as a sublimited endorsement with limits of $25,000 to $250,000, far below the potential loss from a successful deepfake executive fraud attack that targets large wire transfers. Verify the specific social engineering coverage terms, sublimit, and verification procedure requirements in any policy you are evaluating or renewing. If the sublimit is significantly below your maximum single wire transfer authorization amount, negotiating a higher sublimit is a priority.

The war exclusion remains a contested area for AI-driven attacks that may have nation-state sponsorship or origin. Some carriers have specifically modified their war exclusion language to clarify that cyber operations sponsored by nation-states are not automatically excluded unless they rise to the level of an act of war in the traditional military sense. Review your policy's war exclusion language with your broker annually to understand its scope and potential application to the threat types your industry faces.

Social Engineering and Funds Transfer Fraud Coverage

Given the prominence of social engineering and deepfake fraud as financial loss drivers in 2026, specifically evaluating and negotiating for adequate social engineering fraud coverage has become a priority in cyber insurance program design for businesses of any size. Social engineering fraud coverage pays for direct financial losses resulting from employees being deceived into transferring funds to fraudulent accounts through manipulation or impersonation rather than technical system compromise. When evaluating social engineering coverage, the key parameters to assess are the coverage sublimit relative to your potential exposure from a single incident, the verification procedure requirements that must be satisfied for coverage to apply, and whether the coverage applies to payments initiated by your employees based on both executive impersonation and vendor impersonation scenarios.

How Insurers Are Adapting Underwriting for AI Threats

Cyber insurance underwriters in 2026 are asking more specific questions about AI threat-related controls as part of the standard application and renewal process. Beyond the now-standard MFA requirement, underwriters are increasingly asking about identity and access management programs, endpoint detection and response capabilities, and incident response plan testing frequency. Questions specifically related to social engineering controls are becoming more common. Underwriters ask about callback verification requirements for wire transfers and payment changes, whether vendor banking information changes require secondary verification through out-of-band communication, and whether employees have received specific training on voice and video deepfake detection and verification procedures. Businesses that can affirmatively document these controls receive better underwriting terms than those that cannot.

Controls That Reduce Both Deepfake Risk and Insurance Premiums

Establishing a mandatory callback verification process for all wire transfers above a defined threshold, requiring the callback to use a phone number from your established vendor or banking contact records rather than any number provided in the transaction request, prevents the majority of business email compromise and deepfake voice fraud attacks. Multi-person authorization for wire transfers above threshold amounts eliminates single-point failure in the authorization process. An attacker who successfully deceives one employee through deepfake impersonation still faces a second required approver who independently confirms the legitimacy of the transaction through the established verification process. Training employees specifically on deepfake technology, what it looks and sounds like, and the verification procedures that defeat it is increasingly important as these attacks become more common and more technically convincing.

The Future of Business Cyber Insurance

The trajectory of AI-driven cyber threats suggests the pace of attack evolution will continue to outrun defensive adaptation in the near term, keeping cyber risk elevated and cyber insurance important for businesses of all sizes. Insurers are investing heavily in their own AI-driven underwriting and claims tools to better assess risk in real time, provide policyholders with actionable security guidance, and respond more efficiently to the increasing volume of cyber claims. The market is moving toward more coverage differentiation between businesses with strong, documented cybersecurity programs and those with minimal controls. Businesses that demonstrate mature security practices through documented controls, regular training, incident response planning, and third-party security assessments will increasingly access premium discounts and broader coverage terms that are simply not available to businesses with undifferentiated minimal control environments.

Understanding Certificate of Insurance Requirements

A Certificate of Insurance, commonly called a COI or ACORD certificate, is a standardized document that provides summary evidence of an insurance policy's existence and key terms. Clients, landlords, general contractors, event venues, and government agencies routinely require businesses to provide a COI as a condition of doing business, signing a lease, or obtaining a permit. Understanding what a COI contains, what it represents, and what it does not promise is important for business owners on both sides of this requirement.

A standard ACORD 25 certificate shows the insured's name and address, the insurance companies providing coverage, the types of coverage in force, the policy numbers, the effective and expiration dates, and the coverage limits for each policy type. It also shows any additional insured endorsements and any certificate holder who must be notified of policy cancellation. The bottom of the certificate typically contains language clarifying that the certificate is for informational purposes only and does not amend, alter, or extend the coverage provided by the policies shown.

For business owners who are asked to provide a COI, contact your commercial insurance broker or agent. Your insurer can typically produce a COI within 24 to 48 hours. If the requesting party requires specific language about additional insured status or waiver of subrogation, your agent must add these endorsements to the underlying policy, which may take additional time and may involve an additional premium. Agree to these endorsement requirements with your insurer before committing to contractual terms with a client that require them.

For business owners who require COIs from vendors and subcontractors before allowing them to work on their property or projects, establish a tracking system that captures each COI, its expiration date, and a reminder to request renewal before expiration. An expired COI provides no protection, and a vendor operating with lapsed coverage while on your property creates liability exposure for your business if that vendor causes injury or damage during the gap period.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.