A Business Owners Policy, universally called a BOP, is the most efficient starting point for small business commercial insurance. By bundling general liability, commercial property, and business interruption coverage into a single package policy designed for small and medium-sized businesses, the BOP provides more comprehensive protection at a lower price than purchasing each component separately. For the majority of small businesses in eligible industries and size classes, a BOP is the correct foundation for their commercial insurance program and the most important single insurance decision they make.

This guide explains exactly what a BOP covers, what it costs in 2026, what critical coverages it does not include, which businesses qualify for BOP coverage, and how to build a complete insurance program on the BOP foundation by adding the supplemental coverages your specific business operations actually require.

In This Article

- What a BOP Includes

- General Liability Coverage in the BOP

- Commercial Property Coverage in the BOP

- Business Interruption Coverage in the BOP

- What a BOP Costs in 2026

- Who Qualifies for a BOP

- What a BOP Does NOT Include

- Key Add-Ons to Consider

- BOP vs Separate Policies: When Each Makes Sense

- How to Buy a BOP

What a Business Owners Policy Includes

The BOP combines three core commercial insurance coverages that small businesses nearly universally need. General liability insurance protects against third-party claims of bodily injury and property damage arising from your business operations and premises. Commercial property insurance covers damage to your business property including your building if you own it, your business equipment, furniture, inventory, and improvements you have made to a leased space. Business interruption insurance, sometimes called business income coverage, covers the income your business loses and the continuing fixed operating expenses it incurs when a covered property damage event forces you to halt or reduce operations temporarily.

The efficiency of the BOP comes from two sources: the packaging discount that produces better pricing than purchasing each coverage separately from the same or different carriers, and the administrative simplicity of managing a single policy with a single billing cycle, single renewal date, and single point of contact for service. For small businesses with limited administrative resources and a preference for simplicity, the single-policy structure of the BOP has genuine value beyond the direct premium savings it provides.

General Liability Coverage in the BOP

The general liability component of a standard BOP provides coverage for bodily injury and property damage claims arising from your business premises and operations, personal and advertising injury claims including defamation and copyright infringement in advertising, products and completed operations claims for injury or damage caused by your products or completed work after they have left your control, and medical payments coverage for minor injuries sustained by customers or visitors on your premises regardless of whether you were at fault.

Standard BOP general liability limits are typically $1,000,000 per occurrence and $2,000,000 aggregate. These are the minimums most commercial leases require and the limits most client contracts specify as a condition of doing business with them. Higher limits of $2,000,000 per occurrence and $4,000,000 aggregate are available and appropriate for businesses with greater exposure from their specific operations. Commercial umbrella coverage can extend these limits further for businesses with significant asset exposure or that face contractual requirements for higher liability limits from their largest clients.

Commercial Property Coverage in the BOP

The commercial property component covers physical damage to your business property caused by covered perils including fire, lightning, windstorm and hail, explosion, riots, aircraft and vehicle impact, smoke, vandalism, and sprinkler leakage. The coverage includes your building if you own it, your business personal property including furniture, equipment, computers, tools, and inventory whether at your business location or temporarily off-premises, and improvements and betterments you have made to a leased space that you have a financial interest in protecting.

Commercial property in a BOP is typically written on a replacement cost value basis, meaning the insurer pays to replace covered property with new property of like kind and quality without depreciation adjustment. This is superior to actual cash value coverage, which deducts depreciation and can leave you significantly undercompensated for older equipment and furnishings. Always verify that your BOP property coverage is written on a replacement cost value basis rather than actual cash value before assuming the coverage amount stated is what you would actually receive in a total loss claim.

Setting the property coverage limit accurately is the most important decision in structuring the property component. The coverage limit should reflect the total replacement cost of all business property at the covered location, including all contents, equipment, inventory at peak stocking levels, and tenant improvements you have made to the space. Underestimating this figure creates a co-insurance gap that reduces claim payments proportionally to the degree your coverage limit falls below the actual replacement value.

Business Interruption Coverage in the BOP

Business interruption coverage pays for the income your business loses and the fixed operating expenses you continue to incur when a covered property damage event forces you to halt or reduce operations. If a fire destroys your restaurant's kitchen and you must close for four months while it is rebuilt, business interruption coverage pays your lost net income during the closure period plus continuing fixed expenses like rent, loan payments, insurance premiums, and utilities that continue even when you are not generating revenue.

The business interruption coverage limit should be set based on your business's actual monthly revenue and the realistic maximum period during which you might need coverage while repairs are completed. A coverage period of 12 months is standard and adequate for most businesses. Businesses in industries with complex rebuilding processes, specialized equipment with long lead times for replacement, or unique facilities that are difficult to replicate quickly should consider extended coverage periods of 18 or 24 months. Business interruption coverage that runs out before repairs are complete leaves the business to absorb subsequent income losses with no insurance support.

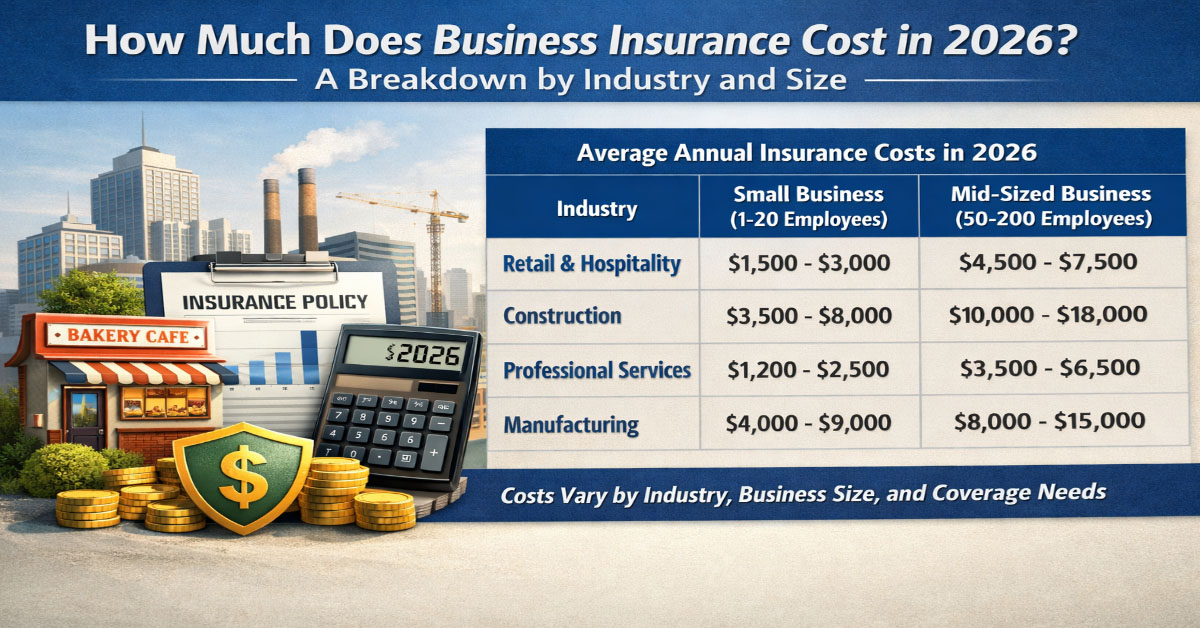

BOP Cost by Business Type: 2026 Estimates

Who Qualifies for a BOP

BOPs are designed for small to medium-sized businesses in standard commercial risk categories. Insurer eligibility criteria for BOP placement typically include revenue under a specified threshold of $5,000,000 to $10,000,000 depending on the carrier and industry, premises size within specified square footage limits, operations classified in eligible industry categories, and a limited geographic footprint. Most retailers, offices, small service businesses, apartments, small warehouses, small restaurants, and light manufacturing operations qualify for BOP placement. Businesses in high-hazard categories including large contractors, heavy manufacturing, transportation, farming, and certain hospitality operations typically do not qualify and require commercial package policies or standalone placements instead.

What a BOP Does NOT Include

Understanding the coverages the BOP does not include is as important as understanding what it does include, because the gaps represent financial exposures that require separate coverage decisions. Workers compensation insurance for employee injuries is universally excluded from BOPs and is required separately in virtually every state for businesses with employees. Professional liability insurance for claims arising from professional services errors is excluded from standard BOPs and must be purchased separately. Cyber liability insurance for data breaches and cyberattacks is excluded from standard BOPs, though some carriers now offer limited cyber endorsements as an add-on. Commercial auto insurance for vehicles used in business operations is excluded. Health insurance, life insurance, and disability insurance for owners and employees are not commercial property and casualty products and are not part of the BOP framework.

Key Add-Ons to Build on the BOP Foundation

Once the BOP provides the foundational coverage, identifying and adding supplemental coverages most relevant to your specific business operations completes the insurance program. For businesses with professional services exposure, professional liability insurance is the highest priority add-on. For any business with employees, workers compensation is legally required in most states. For any business that handles customer or employee data digitally, cyber liability insurance is increasingly essential and should not be treated as optional. For businesses that use vehicles in operations, commercial auto coverage is required. For businesses with significant liability exposure from the scale or nature of their operations, an umbrella policy provides additional limits protection at relatively low cost per dollar of additional coverage.

BOP vs Separate Policies

For most small businesses in eligible industries, the BOP produces better pricing and simpler administration than purchasing separate general liability and commercial property policies. The bundling discount that carriers offer for BOP placement typically represents 10 to 15 percent savings compared to separate policy pricing for the same underlying coverages. Separate standalone policies become appropriate when a business's needs in a specific coverage area exceed what the BOP framework accommodates or when the business does not qualify for BOP placement due to size, revenue, or operations type.

How to Buy a BOP

BOPs are available from most major commercial insurers through direct channels, independent agents, and online broker platforms. For straightforward businesses in standard risk categories, online BOP quoting platforms including Next Insurance, Hiscox, The Hartford, State Farm commercial, and Nationwide allow small businesses to get quotes and purchase coverage without agent involvement. For businesses with more complex needs, in unusual industries, or with claims history, working with an independent commercial insurance broker who can access multiple carriers typically produces better outcomes than direct channel purchasing alone.

When purchasing a BOP, verify that the coverage limits for all three components are set appropriately for your actual business rather than at defaults or minimums. Adequate general liability limits for the scale of your customer interaction and operations, a property coverage limit that reflects the true replacement cost of all business contents and improvements, and a business interruption coverage limit and period that reflects your actual monthly revenue and realistic restoration timeline are all essential. Low limits that appear to save premium create financial gaps that make the savings not worth having when a major claim requires the coverage to actually perform.

Understanding Certificate of Insurance Requirements

A Certificate of Insurance, commonly called a COI or ACORD certificate, is a standardized document that provides summary evidence of an insurance policy's existence and key terms. Clients, landlords, general contractors, event venues, and government agencies routinely require businesses to provide a COI as a condition of doing business, signing a lease, or obtaining a permit. Understanding what a COI contains, what it represents, and what it does not promise is important for business owners on both sides of this requirement.

A standard ACORD 25 certificate shows the insured's name and address, the insurance companies providing coverage, the types of coverage in force, the policy numbers, the effective and expiration dates, and the coverage limits for each policy type. It also shows any additional insured endorsements and any certificate holder who must be notified of policy cancellation. The bottom of the certificate typically contains language clarifying that the certificate is for informational purposes only and does not amend, alter, or extend the coverage provided by the policies shown.

For business owners who are asked to provide a COI, contact your commercial insurance broker or agent. Your insurer can typically produce a COI within 24 to 48 hours. If the requesting party requires specific language about additional insured status or waiver of subrogation, your agent must add these endorsements to the underlying policy, which may take additional time and may involve an additional premium. Agree to these endorsement requirements with your insurer before committing to contractual terms with a client that require them.

For business owners who require COIs from vendors and subcontractors before allowing them to work on their property or projects, establish a tracking system that captures each COI, its expiration date, and a reminder to request renewal before expiration. An expired COI provides no protection, and a vendor operating with lapsed coverage while on your property creates liability exposure for your business if that vendor causes injury or damage during the gap period.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.