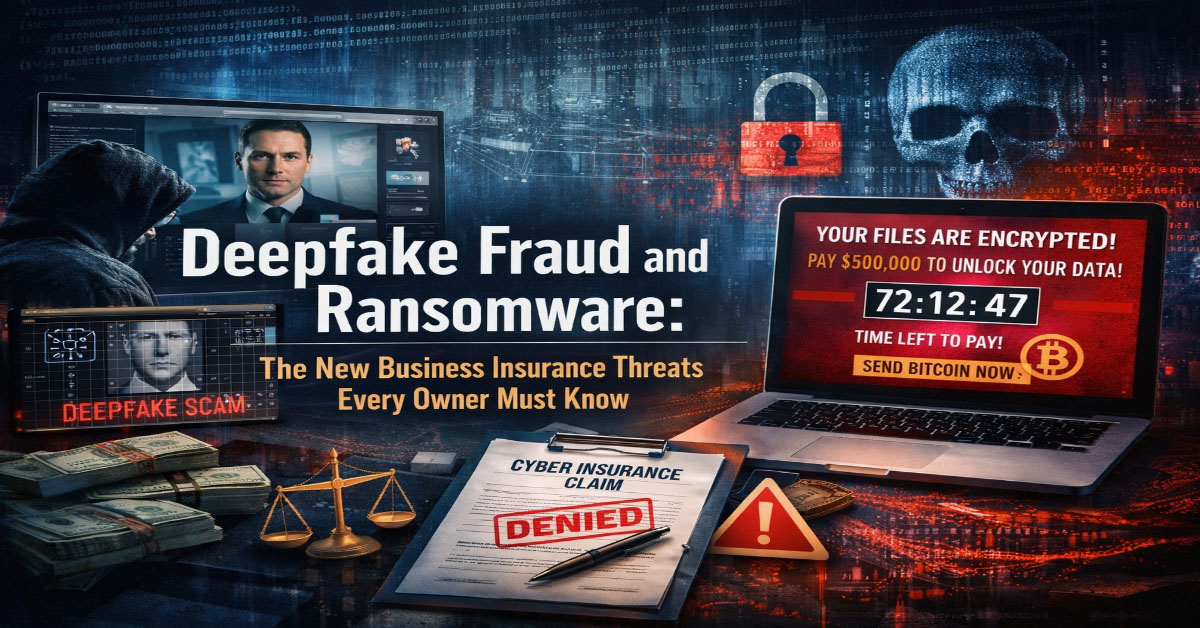

Small and medium-sized businesses are targeted in 43 percent of all cyberattacks, yet less than half carry any cyber insurance. The average ransomware payment demanded from small businesses reached $400,000 in 2025. A single data breach involving customer payment information can trigger notification requirements in multiple states, legal fees, regulatory fines, forensic investigation costs, and customer notification expenses that collectively run $100,000 to $500,000, an amount that would be existential for most small businesses operating without cyber coverage.

In 2026, cyber insurance has crossed from a niche product for large enterprises into a standard component of responsible small business risk management. This guide covers what cyber insurance actually covers, what policies realistically cost for different business sizes and industries, how underwriting works, and how to choose coverage that genuinely matches your business's risk exposure.

In This Article

- Why Small Businesses Are Primary Targets

- What Cyber Insurance Covers

- First-Party vs Third-Party Coverage

- What Cyber Insurance Costs in 2026

- How Cyber Underwriting Works

- Most Common Small Business Cyber Claims

- How to Choose the Right Coverage

- Key Exclusions to Watch For

- Cybersecurity Controls That Reduce Premiums

- Top Cyber Insurance Carriers for Small Business

Why Small Businesses Are Primary Targets in 2026

The targeting of small businesses by cybercriminals is not random. It is economically rational from the attacker's perspective. Small businesses typically hold valuable data including customer payment information, employee personally identifiable information, and business financial records. They typically operate with smaller IT budgets, less sophisticated security infrastructure, fewer dedicated security personnel, and less rigorous employee security training than large enterprises. They are also frequently connected to larger enterprise customers or supply chains through vendor access credentials and data integrations, making them a back-door entry point to larger, more lucrative targets.

The ransomware attack model has evolved in 2026 into a more sophisticated double extortion approach. Attackers encrypt the victim's data to disable operations while simultaneously exfiltrating a copy of sensitive files. They then demand ransom both to provide the decryption key and to prevent publishing the exfiltrated data publicly. This double leverage dramatically increases the pressure on victims to pay and has driven average ransom demands significantly higher than the earlier encryption-only model.

Business email compromise, in which attackers impersonate executives, vendors, or clients through fraudulent emails to redirect wire transfers or obtain sensitive information, has surpassed ransomware as the most financially costly cyber threat for many small businesses in dollar terms. BEC attacks require no technical exploitation of systems; they exploit human judgment through convincing impersonation and can create direct financial losses reaching six figures in a single incident with no warning.

Cyber Threat Landscape: Small Business Data 2026

What Cyber Insurance Covers

Cyber insurance policies cover two broad categories of losses: first-party losses that directly affect your business and third-party losses that affect others as a result of a breach or attack on your systems. Understanding both categories and ensuring your policy adequately addresses both is essential for comprehensive protection against the full range of cyber risk your business faces.

First-party coverages pay for costs your business incurs directly as a result of a cyber incident. These typically include business interruption losses from network downtime preventing normal operations, data restoration costs to recover or recreate lost or corrupted data, ransomware payment costs and the negotiation support that facilitates those payments, forensic investigation costs to determine how the breach occurred and what was affected, notification costs for complying with state and federal breach notification requirements, credit monitoring services provided to affected customers or employees as required by notification laws, and public relations costs to manage reputational damage from public disclosure of a breach.

Third-party coverages pay for your liability to others who are harmed by a cyber incident affecting your business. These include legal defense costs in privacy liability lawsuits brought by customers, employees, or regulators whose data was compromised; regulatory fines and penalties under state privacy laws like the California Consumer Privacy Act, under GDPR for businesses with European data subjects, and under HIPAA for healthcare-adjacent businesses handling protected health information; and payment card industry fines and assessments from card networks following a payment card data breach.

First-Party vs Third-Party Coverage in Practice

Understanding which specific incidents trigger first-party versus third-party coverage helps you evaluate whether a given policy adequately addresses your business's specific risk profile. A ransomware attack that encrypts your files and halts operations for two weeks is primarily a first-party event: the business interruption loss, ransom payment, forensic investigation, and data restoration are all first-party costs. If the same attack also exfiltrated customer data, it becomes a combined event triggering both first-party and third-party coverages simultaneously.

A business email compromise incident that results in an unauthorized wire transfer is primarily a first-party crime coverage event rather than a traditional cyber liability event. Not all cyber insurance policies include social engineering or funds transfer fraud coverage, which is a significant gap for businesses exposed to BEC risk. Verify explicitly whether your cyber policy includes social engineering fraud coverage and at what sublimit, as this is increasingly a standalone coverage requirement for the most common financial loss event facing small businesses in 2026.

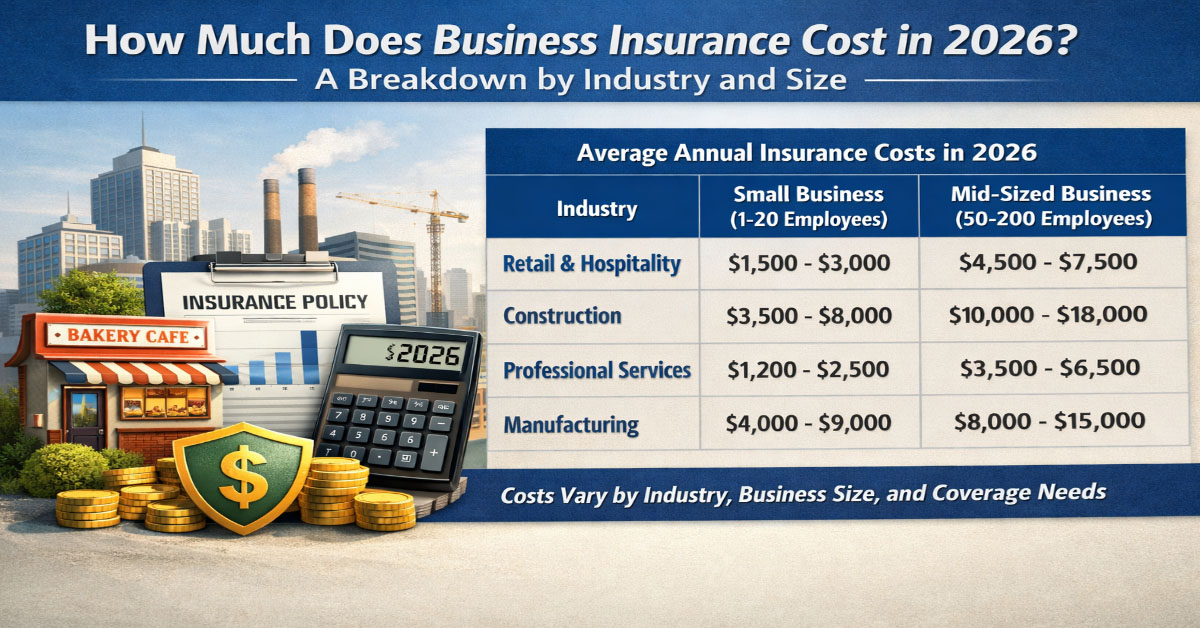

What Cyber Insurance Costs for Small Businesses in 2026

Cyber insurance pricing in 2026 reflects the elevated claim frequency and severity of recent years combined with improved underwriting sophistication that allows carriers to price different risk profiles more precisely than was possible when the product was newer. A very small business with annual revenue under $500,000, minimal customer data, and basic cybersecurity controls can obtain $1,000,000 in cyber coverage for approximately $52 to $80 per month. A small professional services firm with revenue of $1,000,000 to $5,000,000 carrying customer payment information and relying on technology for primary operations can expect $150 to $400 per month for $1,000,000 in coverage. A small healthcare or financial services business with sensitive regulated data can pay $500 to $1,500 per month or more for adequate coverage at higher limits.

Premiums have stabilized somewhat in 2026 after the dramatic increases of 2021 and 2022, when a wave of large ransomware incidents drove many carriers to sharply increase rates and tighten underwriting requirements. The market is now more differentiated: businesses with strong cybersecurity controls receive meaningfully more competitive pricing than those with minimal controls, creating a direct financial incentive for security investment beyond the risk reduction benefit alone.

How Cyber Underwriting Works in 2026

Cyber insurance underwriting has become significantly more rigorous. The application for a small business cyber policy now includes detailed questions about specific security controls rather than general representations about security posture. The controls most commonly asked about and most heavily weighted in underwriting decisions include multifactor authentication for email, remote access, and administrative accounts; endpoint detection and response software on all company devices; offline or immutable backup systems that cannot be encrypted by ransomware; privileged access management limiting which accounts have administrative rights; security awareness training frequency including phishing simulations; and incident response plan existence and testing history.

The presence or absence of multifactor authentication is a binary underwriting criterion at many carriers in 2026. Businesses that cannot confirm MFA on email and remote access systems are either declined for standard market coverage or face significant premium surcharges. This directly reflects the reality that the vast majority of successful ransomware and BEC attacks involve credential compromise that properly implemented MFA would have blocked. If your business lacks MFA on these systems, implementing it is the single highest-priority cybersecurity action from both a risk management and an insurability standpoint.

Most Common Small Business Cyber Claims

Ransomware and extortion remains the most costly claim category by dollar value. A successful ransomware attack that halts operations for one to three weeks generates business interruption losses, forensic investigation costs, and potentially ransom payment costs that can reach $50,000 to $300,000 for a small business even before any third-party notification costs are included. The recovery complexity is significant: simply paying the ransom does not guarantee full operational restoration, and many businesses that pay find that data corruption, persistent backdoors, or incomplete decryption require substantial additional system rebuild work beyond the ransom payment itself.

Business email compromise and social engineering fraud generate the most claims by frequency. An attacker impersonating an executive convinces an employee to wire funds to a fraudulent account. Or an attacker impersonating a vendor submits fraudulent invoice payment instructions. These incidents typically produce direct financial losses of $20,000 to $150,000 per incident and are not covered under standard commercial crime policies unless a specific cyber or social engineering endorsement is included.

Data breaches involving customer personal information trigger notification obligations under 50 different state laws with varying requirements. The average cost of complying with these notification requirements for a small business breach involving a few thousand customer records runs $25,000 to $80,000 in legal fees, notification mailing costs, and credit monitoring services even without any accompanying litigation from affected individuals or regulatory investigation.

How to Choose the Right Cyber Coverage

Selecting cyber insurance requires matching the coverage structure to your specific business's risk profile rather than simply purchasing the cheapest available policy. The key parameters to evaluate include the specific first-party coverages included in the base policy versus available endorsements, the sublimits that apply to specific loss categories particularly ransomware payments, social engineering fraud, and regulatory fines, the retroactive date which determines how far back a cyber incident can have originated and still be covered under the current policy, and the specific definition of covered events which in some policies excludes certain attack types or vectors.

For businesses that handle payment card information, confirm that the policy explicitly covers PCI DSS fines and forensic investigation costs associated with a payment card breach. For healthcare adjacent businesses handling any protected health information, confirm HIPAA regulatory coverage is included without a sublimit that would be inadequate given HHS enforcement penalty ranges. For businesses with significant reliance on cloud services, confirm that cloud service outages and third-party infrastructure failures trigger business interruption coverage under the policy's specific terms rather than being excluded as dependent business interruption losses.

Key Exclusions to Watch For

Several common exclusions create significant coverage gaps for specific businesses. The war exclusion, which excludes losses from nation-state cyberattacks, has generated significant litigation since the NotPetya attacks of 2017 and remains a contested area in cyber insurance. Verify how your specific policy defines the war exclusion and whether it creates meaningful exposure for your business given your industry and the types of threat actors most likely to target organizations like yours.

The prior knowledge exclusion prevents coverage for incidents the insured had knowledge of before the policy inception date. The verification procedure exclusion can deny social engineering fraud coverage if required callback verification procedures were not followed before a wire transfer was made. Unencrypted device exclusions can deny coverage for data breaches involving personal information on unencrypted laptops or portable storage. Understanding and operationalizing the requirements these exclusions impose is as important as understanding what the policy covers.

Cybersecurity Controls That Reduce Premiums

Implementing specific cybersecurity controls produces both direct risk reduction and meaningful premium discounts from cyber insurers who now explicitly price these controls into their underwriting models. Multifactor authentication on all user accounts is the single highest-impact control for both security and insurability. Endpoint detection and response software on all company devices provides behavioral monitoring that detects and stops attacks in progress rather than relying solely on signature-based antivirus. Regular offline or cloud-based backups that cannot be encrypted by ransomware ensure business continuity even if primary systems are compromised. Documented employee security awareness training conducted at least annually reduces the BEC and social engineering risk that drives a large share of small business cyber losses. Each of these controls, when confirmed during the underwriting process, produces premium reductions that typically exceed the cost of implementing the control, making security investment self-funding through insurance savings in many cases.

Top Cyber Insurance Carriers for Small Business

Coalition and At-Bay are cyber-specialist carriers that have built their business model entirely around cyber risk and offer both insurance coverage and active risk management tools including vulnerability scanning and threat intelligence to policyholders. Cowbell is another cyber-specialist insurer with an AI-powered underwriting platform that prices risk more dynamically than traditional carriers. Traditional insurers including Hartford, Travelers, Chubb, AIG, and Beazley all have robust cyber programs with strong claims handling infrastructure accumulated over years of managing complex cyber claims. For small businesses, cyber-specialist carriers often offer more competitive pricing and better-tailored coverage structures, while traditional carriers may offer better integration with existing commercial insurance programs through a broker relationship that manages multiple coverage lines.

Understanding Certificate of Insurance Requirements

A Certificate of Insurance, commonly called a COI or ACORD certificate, is a standardized document that provides summary evidence of an insurance policy's existence and key terms. Clients, landlords, general contractors, event venues, and government agencies routinely require businesses to provide a COI as a condition of doing business, signing a lease, or obtaining a permit. Understanding what a COI contains, what it represents, and what it does not promise is important for business owners on both sides of this requirement.

A standard ACORD 25 certificate shows the insured's name and address, the insurance companies providing coverage, the types of coverage in force, the policy numbers, the effective and expiration dates, and the coverage limits for each policy type. It also shows any additional insured endorsements and any certificate holder who must be notified of policy cancellation. The bottom of the certificate typically contains language clarifying that the certificate is for informational purposes only and does not amend, alter, or extend the coverage provided by the policies shown.

For business owners who are asked to provide a COI, contact your commercial insurance broker or agent. Your insurer can typically produce a COI within 24 to 48 hours. If the requesting party requires specific language about additional insured status or waiver of subrogation, your agent must add these endorsements to the underlying policy, which may take additional time and may involve an additional premium. Agree to these endorsement requirements with your insurer before committing to contractual terms with a client that require them.

For business owners who require COIs from vendors and subcontractors before allowing them to work on their property or projects, establish a tracking system that captures each COI, its expiration date, and a reminder to request renewal before expiration. An expired COI provides no protection, and a vendor operating with lapsed coverage while on your property creates liability exposure for your business if that vendor causes injury or damage during the gap period.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.