Business insurance costs vary dramatically by industry, coverage type, business size, location, and claims history. A restaurant in Chicago pays very different premiums than a software consulting firm in the same building. A landscaping company carries a very different risk profile than an accounting practice with identical annual revenue. Understanding what businesses in your industry actually pay for insurance, what factors drive those costs up or down, and how to manage your specific premium is practical financial knowledge that directly affects your profitability.

This guide breaks down business insurance costs in 2026 by coverage type and industry category, explains the underwriting factors that most significantly affect pricing, and provides actionable strategies for reducing your insurance spend without creating dangerous coverage gaps that leave your business exposed to risks you cannot afford to absorb.

In This Article

- The Core Business Insurance Coverage Types

- What Each Coverage Type Costs in 2026

- Costs by Industry Category

- What Drives Business Insurance Costs Higher

- How to Reduce Your Business Insurance Costs

- How Claims History Affects Premium

- How to Shop for Business Insurance Effectively

- Common Small Business Insurance Mistakes

The Core Business Insurance Coverage Types

Most small businesses need a core set of insurance coverages that address different categories of financial risk exposure. General liability insurance covers claims of bodily injury and property damage by third parties arising from your operations, premises, and products. Commercial property insurance covers damage to your business property, equipment, and inventory from covered perils. Business interruption insurance covers lost income when operations are halted by a covered property damage event. Workers compensation insurance is legally required in virtually every state for businesses with employees and covers employee injuries and occupational illnesses. Professional liability or errors and omissions insurance covers claims arising from professional services errors, omissions, or failure to deliver as promised. Commercial auto insurance covers vehicles used in business operations. Cyber liability insurance covers losses from cyberattacks, data breaches, and social engineering fraud. Umbrella or excess liability insurance extends the limits of your primary liability policies for catastrophic claims that exceed base policy limits.

The specific combination of coverages a business needs depends on its operations, industry, number of employees, property owned or leased, and risk profile. Understanding what each coverage type costs and what it actually protects against allows a business owner to make informed decisions about which coverages are essential, which are highly advisable, and which might be deferred or declined based on actual risk assessment rather than habit.

What Each Coverage Type Costs for Small Businesses in 2026

Average Annual Business Insurance Costs: 2026 Estimates

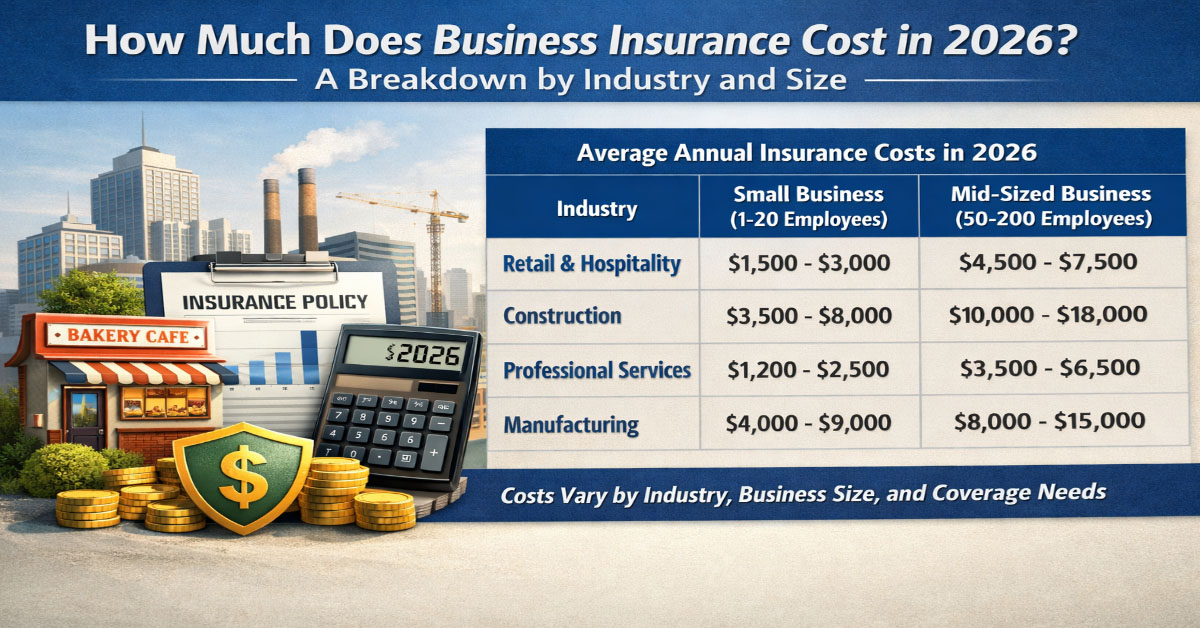

Business Insurance Costs by Industry Category

Retail and Restaurant

Retail stores face moderate general liability exposure from customer premises liability and product-related claims. A small retail store with annual revenue under $500,000 and no delivery operations typically pays $800 to $2,000 per year for a BOP. A restaurant adds the complications of food contamination exposure, liquor liability if alcohol is served, and higher slip-and-fall frequency due to kitchen spills and foot traffic patterns, producing BOP costs of $2,000 to $6,000 per year depending on revenue and alcohol service volume. Workers compensation for food service operations runs $2 to $4 per $100 of payroll, adding $2,000 to $8,000 annually for a small restaurant with 10 to 20 employees.

Contractors and Tradespeople

Contractors face elevated general liability exposure from the physical nature of their work and the potential for significant property damage or bodily injury at client sites. General liability for a small general contractor with $500,000 in annual revenue typically runs $2,000 to $5,000 per year. Workers compensation for construction trades is among the highest rate classes in the market, often $5 to $15 per $100 of payroll depending on the specific trade and state, representing a substantial portion of total insurance costs for labor-intensive construction businesses. A roofing contractor with $1,000,000 in payroll may pay $70,000 to $150,000 annually in workers compensation premiums alone, which must be factored into pricing to maintain profitability.

Professional Services

Accounting firms, law firms, consulting practices, and similar professional services businesses have lower general liability exposure from their office-based operations but significant professional liability exposure from the expert advice they provide. A small accounting practice with five employees and $1,000,000 in annual revenue might pay $500 to $800 for general liability, $2,000 to $4,000 for professional liability, $3,000 to $6,000 for workers compensation, and $800 to $1,500 for commercial property, for a total annual insurance spend of approximately $6,300 to $12,300 depending on specific carrier pricing and coverage levels.

Technology Companies

Technology businesses including software development firms, IT consultants, managed service providers, and SaaS companies have a distinctive risk profile combining professional liability exposure for technology errors and omissions, significant cyber liability exposure for data handling and system security responsibilities, and modest general liability exposure from primarily office-based operations. A small technology firm with $2,000,000 in annual revenue might pay $2,000 to $5,000 for technology E and O, $2,000 to $6,000 for cyber liability, $500 to $1,000 for general liability, and $4,000 to $8,000 for workers compensation, totaling $8,500 to $20,000 per year for a comprehensive commercial insurance program.

Healthcare Adjacent Businesses

Businesses that work with or handle health-related data, provide any healthcare services, or operate in the healthcare supply chain face elevated cyber liability premiums due to HIPAA requirements and the high value of healthcare data in breach scenarios. A small healthcare IT company or medical billing service can face cyber premiums of $5,000 to $20,000 per year for adequate coverage, which represents a significant component of total insurance costs. Medical professionals face malpractice premiums that vary dramatically by specialty, geographic location, and claims history, ranging from $10,000 per year for low-risk specialties to $100,000 or more annually for high-risk surgical specialties in high-litigation states.

What Drives Business Insurance Costs Higher

Claims history is typically the most powerful single pricing factor at renewal. A business with no claims in the past three to five years commands meaningfully better pricing than one with multiple claims regardless of the size of individual claims. The first claim on an otherwise clean record raises rates noticeably. The second claim within three years raises rates dramatically and may trigger non-renewal at some carriers. Workers compensation uses a formal experience modification rate system that directly ties your premium to your claims history over a rolling three-year period; a single large claim can surcharge your premium for three to four years beyond when the claim occurred.

Industry and operations type determine the baseline risk class your business is assigned. Some operations are simply more hazardous than others and are priced accordingly at every revenue level. Business revenue and payroll size directly affect most coverage premiums because they serve as proxies for the scale of operations and the resulting claim exposure. Geographic location affects property insurance through local natural catastrophe exposure and construction cost factors, affects workers compensation through state rate filing requirements, and affects general liability through local litigation environment characteristics that vary substantially between states.

How to Reduce Your Business Insurance Costs

Shopping your coverage at every renewal is the most consistently effective cost management action available. Business insurance pricing varies significantly between carriers for identical risk profiles, and carrier competitive positions shift every year based on their own loss experience, reinsurance costs, and market strategy. Independent commercial insurance brokers who access multiple carriers and have experience in your industry can identify savings opportunities efficiently and present your risk in its most favorable context to underwriters who do not know your business.

Implementing the risk management practices that underwriters use to evaluate your risk class produces both genuine risk reduction and premium discounts. For contractors, safety programs, OSHA compliance documentation, and diligent claims management that produces a favorable experience modification rate generate lower workers compensation and general liability premiums year over year. For professional services firms, documented quality assurance processes, engagement letters for all client work, and written scope of work documentation reduce professional liability exposure and may qualify for premium discounts. For all businesses, a claims-free history is the most powerful long-term premium reduction tool available, making every risk management investment doubly valuable.

Bundling multiple coverages with a single insurer through a BOP or commercial package policy typically produces better pricing than purchasing each coverage separately from different carriers. Working with a single commercial insurer or broker relationship that can package coverages comprehensively is usually more cost-effective than piecing together individual policies from multiple sources, as long as the single carrier's pricing is competitive across all coverage lines.

How Claims History Affects Business Insurance Premium

Workers compensation insurance uses the experience modification rating system that directly ties your premium to your claims history over a rolling three-year period. Your experience mod compares your actual claims costs to the expected claims costs for a business of your size and industry classification. An E-mod above 1.0 increases your premium; below 1.0 decreases it. A single large workers compensation claim can affect the E-mod for three to four policy years before it rolls off the experience period. Multiple claims compound the effect dramatically. A business that goes three consecutive years with zero or minimal claims can achieve a very favorable E-mod that provides a meaningful competitive cost advantage over time.

General liability and professional liability pricing also reflects claims history, though typically through a more qualitative underwriting assessment rather than a formal modification factor system. Carriers ask about claims history on renewal applications, and multiple claims within a three to five year window raise rates meaningfully or can result in non-renewal. Maintaining a claims-free record through proactive risk management, careful documentation, and thoughtful decisions about whether to file small claims is a long-term insurance cost reduction strategy with compound financial benefits over time.

How to Shop for Business Insurance Effectively

The most efficient way to shop commercial insurance for a small business is to work with an independent commercial insurance broker who has relationships with multiple carriers, understands your industry, and can present your risk in its most favorable light to underwriters. Unlike personal lines insurance where direct comparison websites work reasonably well for commodity products, commercial insurance requires more nuanced risk presentation that benefits meaningfully from broker expertise and carrier relationships.

When changing insurers or shopping competitively, gather your current policy declarations pages, three to five years of loss runs from your current carrier showing your claims history, your current business financials including annual revenue and payroll by job classification, and any safety programs, certifications, or risk management documentation that demonstrates your risk management quality. Organized and thorough presentation of this information enables underwriters to evaluate your risk accurately rather than applying conservative assumptions to fill information gaps, producing more competitive quotes.

Common Small Business Insurance Mistakes

Carrying inadequate liability limits to save on premium is the most costly small business insurance mistake. General liability limits of $300,000 or less are insufficient for businesses with any meaningful customer interaction or operations that could produce significant injury or property damage claims. A lawsuit arising from a serious customer injury can easily produce a judgment or settlement well above a $300,000 limit, leaving the remainder as direct business liability exposure that can threaten the business's existence. Adequate limits cost only marginally more than inadequate limits and the financial protection they provide is correspondingly much greater per dollar of premium.

Failing to update coverage as the business grows is another common and costly mistake. A business that purchased insurance when it had three employees and $500,000 in revenue and has since grown to fifteen employees and $2,500,000 in revenue without updating its coverage limits may be substantially underinsured across multiple coverage types. Annual review of coverage adequacy against current business size and operations is a basic governance responsibility that pays for itself when a claim occurs and adequate coverage is in place to respond fully.

Understanding Certificate of Insurance Requirements

A Certificate of Insurance, commonly called a COI or ACORD certificate, is a standardized document that provides summary evidence of an insurance policy's existence and key terms. Clients, landlords, general contractors, event venues, and government agencies routinely require businesses to provide a COI as a condition of doing business, signing a lease, or obtaining a permit. Understanding what a COI contains, what it represents, and what it does not promise is important for business owners on both sides of this requirement.

A standard ACORD 25 certificate shows the insured's name and address, the insurance companies providing coverage, the types of coverage in force, the policy numbers, the effective and expiration dates, and the coverage limits for each policy type. It also shows any additional insured endorsements and any certificate holder who must be notified of policy cancellation. The bottom of the certificate typically contains language clarifying that the certificate is for informational purposes only and does not amend, alter, or extend the coverage provided by the policies shown.

For business owners who are asked to provide a COI, contact your commercial insurance broker or agent. Your insurer can typically produce a COI within 24 to 48 hours. If the requesting party requires specific language about additional insured status or waiver of subrogation, your agent must add these endorsements to the underlying policy, which may take additional time and may involve an additional premium. Agree to these endorsement requirements with your insurer before committing to contractual terms with a client that require them.

For business owners who require COIs from vendors and subcontractors before allowing them to work on their property or projects, establish a tracking system that captures each COI, its expiration date, and a reminder to request renewal before expiration. An expired COI provides no protection, and a vendor operating with lapsed coverage while on your property creates liability exposure for your business if that vendor causes injury or damage during the gap period.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.