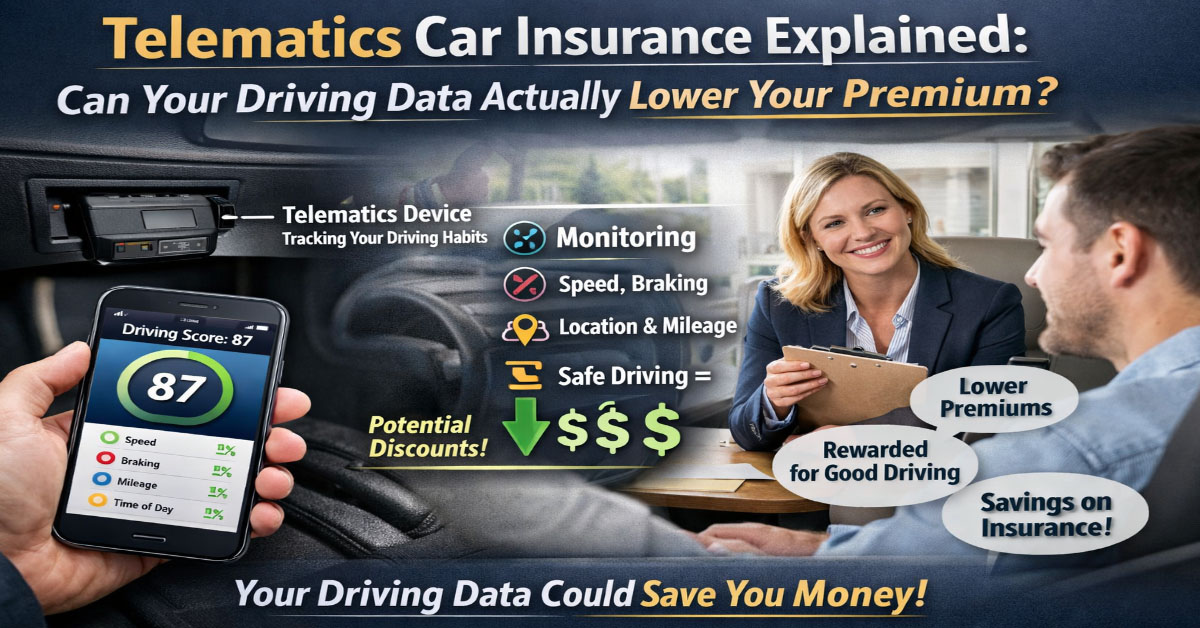

Telematics car insurance, also called usage-based insurance, has moved from a niche experiment to a mainstream option offered by nearly every major U.S. auto insurer. The promise is straightforward: share your driving data, prove you are a safe driver, and earn a lower premium than demographic proxies alone would produce. For the right driver, that promise is real. For others, the trade-off is poor or the program can actually increase your costs.

A Maryland study found that fewer than 31 percent of enrolled drivers actually saved money through their insurer's telematics program. Understanding exactly how these programs work, what they measure, who genuinely benefits, and what you are agreeing to when you enroll is essential before making this decision. This guide covers all of it.

In This Article

- How Telematics Insurance Works

- What Data Is Actually Collected

- How Your Driving Score Is Calculated

- Major Programs Compared

- Who Benefits and Who Does Not

- Privacy: What You Are Agreeing To

- EV Owners and Telematics

- How to Maximize Your Discount

- When to Decline Enrollment

- The Future of Usage-Based Insurance

How Telematics Insurance Works

Telematics insurance collects real-time data about how you actually drive rather than relying solely on demographic proxies like age, gender, marital status, or ZIP code to estimate your risk. The insurer uses one of three collection methods: a smartphone app using GPS, accelerometer, and gyroscope data; a plug-in OBD-II device that connects to your vehicle's diagnostic port; or data accessed directly from the vehicle's manufacturer telematics system through a data-sharing agreement.

The monitoring period varies by program. Some programs monitor continuously throughout your policy period. Others have a defined enrollment window, typically 90 to 180 days, after which the data is used to set a renewal rate adjustment. The driving score calculated during the monitoring period translates into a discount at renewal. Most programs also provide an enrollment discount simply for agreeing to participate, typically 5 to 10 percent, regardless of how your actual driving data scores.

The technology behind modern telematics programs is sophisticated. Smartphone-based systems can distinguish between a driver holding their phone and a passenger holding theirs by analyzing movement patterns and correlating phone position with inferred seat location. They can identify individual driving sessions, map routes precisely, and flag specific moments where behavior deviated from safe norms. The amount of behavioral and locational data collected is substantially more extensive than the simple driving safety question the enrollment discount is framed around.

What Data Is Actually Collected

Speed and Speeding Events

Every program measures how often and by how much you exceed posted speed limits. Treatment of speed varies meaningfully between programs. Some apply penalties for any speed above the posted limit. Others only penalize sustained speeds meaningfully above the limit. Highway driving where traffic routinely flows 5 to 10 miles per hour above the posted limit is treated differently by different programs. Understanding your specific program's thresholds matters if you regularly drive at highway speeds in flow traffic.

Hard Braking

Sudden deceleration above a defined g-force threshold is flagged as a hard braking event. Hard braking is consistently one of the most heavily weighted factors because it correlates with following too closely, distracted driving, and reactive rather than anticipatory driving. The significant limitation is that legitimate situations, including avoiding a pothole, stopping for a child who runs into the street, or yielding to an emergency vehicle, can trigger hard-braking flags that the algorithm cannot distinguish from inattentive braking. Urban drivers who encounter frequent unpredictable traffic conditions are particularly susceptible to accumulating hard-braking events that do not reflect their actual driving quality.

Rapid Acceleration

Aggressive acceleration from stops is penalized across most programs as a proxy for impulsive, aggressive driving that correlates with higher crash risk. Drivers in stop-and-go urban environments accumulate more acceleration events per mile than suburban or rural drivers even if their individual acceleration inputs are comparable. This factor systematically advantages drivers in low-density environments over urban drivers regardless of actual driver quality.

Phone Use While Driving

Smartphone-based programs increasingly detect phone interaction during driving sessions. Definitions of penalized phone use vary by program. Some penalize any detected screen interaction while the vehicle moves above a threshold speed. Others attempt to distinguish purposeful typing from incidental handling. Passenger phone use is a persistent false-positive source for programs that cannot reliably distinguish driver from passenger device activity. This is both the most behaviorally impactful factor for many drivers and the most privacy-sensitive data point collected.

Time of Day Driving

Driving between approximately 11 PM and 4 AM is weighted negatively in most programs because statistical crash risk is higher during these hours due to fatigue and impaired driver presence, even for drivers who are themselves alert and sober. This factor is structurally unfair to night shift workers, emergency responders, hospitality workers, musicians, and others whose employment requires consistent late-night driving. The time-of-day penalty cannot be overcome by safe driving behavior during those hours because the program scores the hour itself, not the quality of driving within it.

Annual Mileage

Total miles driven is tracked and factored into most programs. Lower annual mileage improves scores in most programs because less exposure means lower expected claim frequency. Pay-per-mile programs make mileage the primary pricing variable, which is a different structure from standard telematics programs where mileage is one factor among several behavioral inputs.

Major Telematics Programs: 2026 Comparison

How Your Driving Score Is Calculated

Each carrier uses a proprietary algorithm to translate raw driving data into a composite score. The weights assigned to individual behavioral factors differ between programs. Progressive Snapshot has historically weighted hard braking heavily. State Farm's Drive Safe and Save emphasizes total mileage more prominently. Allstate Drivewise places significant weight on nighttime driving avoidance. Understanding the weighting structure of your specific program before enrolling allows you to evaluate whether your typical driving patterns are likely to score well or poorly given the program's priorities.

The algorithms are continuously refined using the carrier's own claims data correlating driving scores with actual accident outcomes. This means programs that have been operating for several years have more validated scoring models than newer entrants. It also means the weighting can shift between your enrollment period and future renewals as the carrier updates its models based on accumulated data.

One practical implication: a driver who scores poorly on one carrier's program due to, for example, frequent highway driving at speeds slightly above posted limits might score very well on another carrier's program that weights speed less heavily and mileage more favorably. If one telematics program produces a poor or no-discount outcome, evaluating whether a different carrier's program with different weightings would produce a better result for your specific driving profile is worth doing before concluding telematics does not work for you.

Major Programs in Practical Detail

Progressive Snapshot: The Original and Most Consequential

Progressive Snapshot was one of the earliest major telematics programs and remains among the most widely used. It is also the most distinctive for one critical reason: Snapshot is one of the few major programs that can raise your rate at renewal based on poor driving data. Most programs only reward safe driving with discounts and cannot penalize poor driving beyond withholding the discount. Snapshot actively surcharges drivers whose data reveals consistently risky behavior patterns.

This makes the decision to enroll in Snapshot a genuine risk management question rather than simply an upside opportunity. Drivers who are confident their driving data will be favorable should consider it. Drivers who are uncertain, who drive frequently at night, or who have inconsistent braking habits in urban traffic should first consider alternative programs that carry no downside risk.

Liberty Mutual RightTrack: The Lowest-Risk Option

RightTrack's 90-day limited monitoring window in most states is the most consumer-friendly program structure available from a major carrier. You enroll, drive for 90 days, receive a discount based on your performance during that period, and the monitoring ends entirely. Your rate cannot be increased based on the data collected. Maximum discounts of up to 30 percent are real and meaningful. For drivers who want to test whether telematics can save them money without any ongoing surveillance commitment or rate-increase risk, RightTrack is the rational starting point.

State Farm Drive Safe and Save: Convenient and Risk-Free

Drive Safe and Save uses Bluetooth connection to your phone or OnStar and In-Drive connected vehicle systems, making enrollment more seamlessly integrated than plug-in OBD devices. The program cannot raise your rate based on driving data. Maximum discounts of up to 30 percent are achievable for top performers. The program is available in most states and is generally well regarded for transparency about what it measures and how it calculates your score.

Who Benefits and Who Does Not

Ideal Telematics Candidates

The driver who benefits most from telematics drives relatively few miles per year, primarily during daytime hours, with smooth and consistent braking and acceleration habits, and has reason to believe their actual driving behavior is meaningfully safer than their demographic profile suggests to actuarial models. Young drivers in their 20s are perhaps the best candidates because they face high base rates driven by statistical age-group risk data even when they are personally very careful drivers. A 22-year-old who genuinely drives safely can use telematics to break out of the demographic pricing box and pay rates that reflect their actual behavior rather than their age cohort's average.

Low-mileage drivers, remote workers, retirees, and urban residents who primarily use transit but occasionally need a car are also excellent candidates. Their low annual mileage directly improves scores in most programs and reduces the probability of generating penalizing events simply through driving exposure.

Poor Telematics Candidates

Night shift workers, nurses, emergency medical technicians, bartenders, and restaurant staff face a structural disadvantage in most programs that no amount of careful driving can overcome. The time-of-day penalty applies regardless of driving quality during those hours, and it is heavy enough in most program weightings to prevent meaningful discount accumulation even for otherwise excellent drivers.

Dense urban commuters who face frequent stop-and-go traffic, unavoidable emergency braking around pedestrians and cyclists, and high event-per-mile ratios due to traffic density will often score worse than suburban or rural counterparts even if their driving is attentive and skilled. The programs penalize the frequency of braking events without context about why those events occur.

Privacy: What You Are Actually Agreeing To

Before enrolling in any telematics program, reading the specific privacy policy rather than assuming it covers only driving behavior metrics is important. Standard telematics programs collect GPS location data continuously, creating a timestamped log of everywhere your vehicle has been during the monitoring period. This data has been used by insurers in claims investigations to verify or contradict a driver's account of their location at the time of an incident. Multiple cases exist where telematics data contradicted a policyholder's claims statement and contributed to claim denial or reduced settlement.

Most telematics privacy policies permit sharing data with affiliated companies, data aggregators, marketing partners, and other third parties. Some policies allow selling aggregate driving pattern data for commercial purposes including infrastructure planning, automotive research, and marketing targeting. The commercial value of behavioral location data extends well beyond the insurance pricing context in which it is collected, and most consumers are not aware of the full scope of potential uses when they enroll.

EV Owners and Telematics: Special Considerations

EV owners face a unique version of the telematics question. Because EVs are already more expensive to insure, any mechanism that can reduce the base premium deserves careful evaluation. EVs also have more sophisticated onboard telemetry that some insurers can access directly without requiring a separate device or phone app, making enrollment more convenient. Tesla's proprietary insurance product, available in multiple states, uses real-time Safety Score data from the vehicle itself to price coverage month-by-month. Safe Tesla drivers can achieve substantial premium reductions through this program that are sometimes lower than any traditional insurer will offer for the same vehicle.

One specific technical issue for EV owners: regenerative braking systems in many electric vehicles create deceleration profiles that OBD-based and some app-based telematics programs may register as hard-braking events even though the driver used only one-pedal driving without touching the brake pedal. If you drive an EV with regenerative braking capability, verify with the specific program whether its scoring algorithm accounts for regenerative deceleration before assuming your score will accurately reflect your driving behavior.

How to Maximize Your Telematics Discount

If you have evaluated your profile and determined that a telematics program is favorable for your situation, these practices help you earn the maximum available discount rather than settling for average program performance.

Practice genuinely anticipatory driving. Look further ahead when driving and use the space in front of you to coast toward traffic slowdowns rather than maintaining speed until a last-moment brake application. This single habit dramatically reduces hard-braking event frequency, which is typically the most heavily weighted negative factor in most scoring models. Smooth, gradual acceleration from stops eliminates rapid-acceleration events simultaneously.

For phone-based programs, put your phone completely out of reach before starting the vehicle. Turn the screen off, place it face-down in a storage compartment, and set your navigation destination before moving the car. If passengers use their phones during the trip, explain that their phone activity may affect your driving score and ask them to minimize screen interaction while the vehicle is in motion.

If the program measures nighttime driving, reschedule any flexible trips that would naturally fall in the late-night scoring window to daytime where possible, at least during your active monitoring period. Even reducing the proportion of miles driven between 11 PM and 4 AM can meaningfully improve your time-of-day score. This is practical for most drivers during a 90-day monitoring window even if it is not sustainable as a permanent lifestyle modification.

When to Decline Enrollment

Declining telematics enrollment is the right choice if your driving habits include consistent behaviors that score poorly regardless of overall safety, particularly regular nighttime driving. If you are considering Progressive Snapshot specifically, obtain a competing quote from another carrier first. If you can secure a meaningfully better rate elsewhere before the Snapshot discount is factored in, switching may be simpler than gambling on your Snapshot performance with your current insurer.

If you are currently enrolled in a program that can raise rates and your score has been unfavorable, proactively shopping other carriers before your renewal is processed gives you options before a potentially higher rate locks in. The right time to evaluate alternatives is before the renewal, not after receiving a higher rate notice.

The Future of Usage-Based Insurance

Telematics enrollment has grown substantially and continues expanding. TransUnion research found enrollment growing 33 percent year over year in a recent tracking period. Despite this growth, only about 13 to 14 percent of all insured drivers are currently enrolled, leaving enormous room for further adoption if programs continue delivering value to consumers.

Next-generation programs will increasingly access vehicle telemetry directly through manufacturer data-sharing agreements, reducing the friction of app setup or OBD device installation. Artificial intelligence applied to driving data will produce more nuanced assessments that can distinguish a hard-braking event caused by a genuine road hazard from one caused by inattentive following. Embedded pricing, where the vehicle continuously transmits driving data and the insurer adjusts coverage pricing in near-real time, is on the horizon for some manufacturers and insurers.

The long-term direction of auto insurance pricing is clearly toward greater individualization based on demonstrated behavior rather than demographic proxies. Safe drivers who embrace this direction stand to benefit increasingly as the tools become more sophisticated and the market becomes more competitive for favorable driving profiles.

Understanding Your Auto Insurance Declarations Page

Your declarations page, commonly called the dec page, is the single most important document in your auto insurance relationship. It is a one or two page summary of everything your policy covers: the covered vehicles, all named drivers, each coverage type, the limit for that coverage, the deductible, the premium for that coverage, and the total annual premium. Knowing how to read your declarations page is the foundation of any intelligent insurance management decision.

The coverage section lists each coverage type separately: bodily injury liability, property damage liability, medical payments or personal injury protection, uninsured motorist, underinsured motorist, collision, comprehensive, and any endorsements you have added. Each coverage has a premium associated with it. By examining these individually, you can identify which coverages are consuming the largest share of your premium and evaluate whether adjusting them would make sense for your situation.

The limits section shows the maximum the insurer will pay for each coverage category. Bodily injury limits are expressed as a per-person and per-occurrence pair, such as $100,000 per person and $300,000 per occurrence. This means the insurer will pay up to $100,000 for any single injured person and up to $300,000 total for all injured parties from a single accident. Understanding these limits and whether they are adequate for your asset level is one of the most important evaluations you can perform on your current policy.

When you compare quotes from competing carriers, you are comparing their pricing for identical declarations page specifications. Any quote with different limits, deductibles, or coverage inclusions is not a meaningful comparison regardless of how the headline number looks. The discipline of quoting on identical specifications is what separates productive insurance shopping from the experience of switching to a cheaper policy only to discover the coverage gap when a claim occurs.

How Accident Forgiveness Programs Work

Accident forgiveness is an endorsement or program feature offered by many major carriers that waives the premium surcharge for a first at-fault accident within a defined eligibility window. The programs vary significantly between carriers in terms of eligibility requirements, how the forgiveness is earned or purchased, and exactly what is forgiven.

Some carriers include accident forgiveness automatically after three to five years of continuous claim-free coverage with that carrier. Others offer it as a purchasable endorsement add-on. Some programs forgive only the first at-fault accident regardless of severity. Others have damage amount thresholds above which forgiveness does not apply. Understanding the specific terms of your carrier's program before you need it is valuable because the program that sounds like unconditional protection may have conditions that exclude the specific scenario you encounter.

The financial value of accident forgiveness depends on your carrier's standard at-fault surcharge rate and your current premium. If your carrier applies a 35 percent surcharge for three years on a $2,200 annual premium, a single forgiven at-fault accident saves $2,310 in cumulative surcharge costs. The endorsement typically costs $50 to $150 annually. At those numbers, accident forgiveness pays for itself if you have even one at-fault accident during your policy period, making it worth considering particularly for drivers who commute in high-traffic areas or whose household includes younger drivers with statistically higher accident frequencies.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.