Being self-employed is, for many Americans, the ultimate professional freedom. But it comes with one significant complication that employed workers often take for granted: you are entirely responsible for securing your own health insurance, and in 2026, that responsibility has become substantially more financially burdensome following the expiration of enhanced ACA subsidies that previously made marketplace coverage accessible to a much broader range of income levels than the original program design intended.

This guide covers every realistic health insurance option for self-employed individuals in 2026, the self-employed health insurance tax deduction that partially offsets the cost, strategies for managing income to maximize subsidy eligibility, and the specific situations where different approaches make more financial sense for different income levels and household situations.

In This Article

- Your Health Insurance Options as Self-Employed

- ACA Marketplace: The Primary Option

- Maximizing Marketplace Subsidy Eligibility

- The HDHP Plus HSA Strategy

- The Self-Employed Health Insurance Tax Deduction

- Group Coverage Options

- Coverage Through a Spouse's Employer

- Special Enrollment Periods

- Income Management for Subsidy Optimization

- What to Budget for Health Insurance

Your Health Insurance Options as Self-Employed

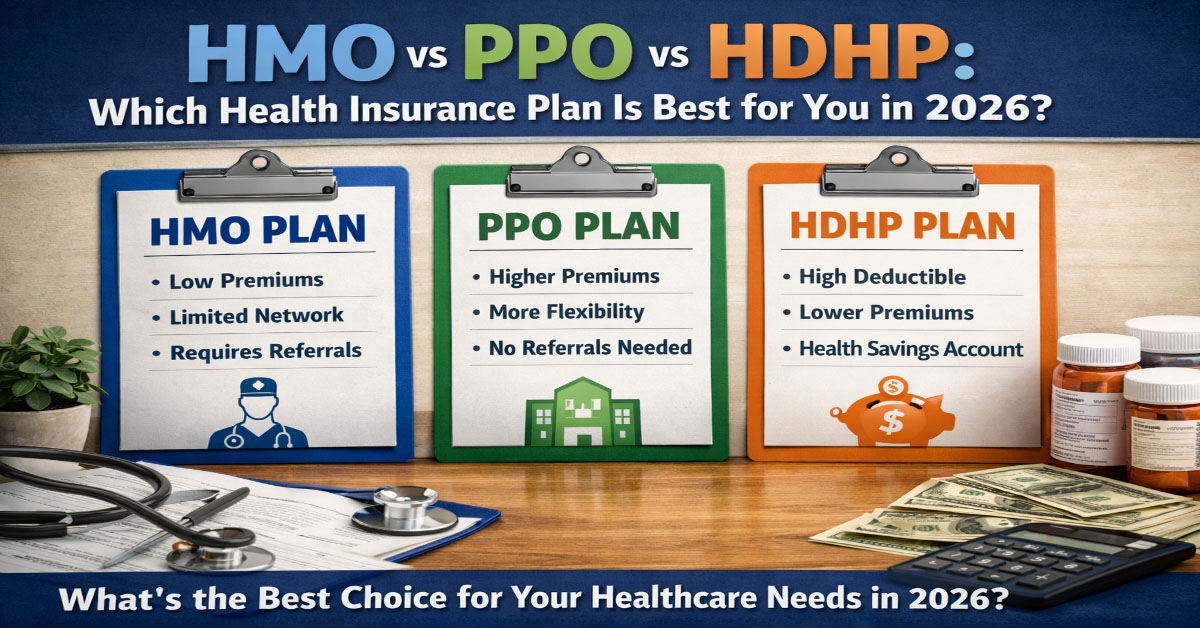

Self-employed individuals in 2026 have several realistic health insurance pathways. The primary options are the ACA individual marketplace, a high-deductible health plan paired with a health savings account, group coverage through professional associations or industry groups that negotiate group rates, coverage through a spouse's employer plan if applicable, COBRA continuation from a previous employer during a transition period, Medicaid if income qualifies, and Medicare if over 65. Each option has different cost structures, eligibility requirements, and coverage characteristics that make it more or less appropriate depending on your specific income level, health status, and household situation. Understanding how these options interact with each other and with the tax code is essential for making the most financially intelligent coverage decision.

ACA Marketplace: The Primary Option for Most Self-Employed

The ACA individual marketplace is the primary coverage source for most self-employed Americans who do not qualify for Medicaid and cannot access group coverage. The marketplace guarantees coverage regardless of pre-existing conditions, requires coverage of essential health benefits, and for those who qualify, provides premium tax credits that reduce monthly costs based on household income relative to the Federal Poverty Level.

In 2026, the elimination of enhanced subsidies has significantly changed the economics of marketplace coverage for higher-income self-employed individuals. The original ACA premium tax credit applies to households with income between 100 and 400 percent of the Federal Poverty Level. For a single self-employed person, that range is approximately $15,060 to $60,240. Households earning above $60,240 now receive zero premium tax credit and must pay the full unsubsidized premium. This cliff creates a genuinely difficult situation for moderately successful self-employed individuals whose business income regularly pushes them above the threshold.

Unsubsidized silver plan premiums for a 45-year-old self-employed individual range from approximately $500 to $700 per month in most markets. For someone in their late 50s, premiums of $700 to $1,000 per month for an individual are common in many states. For self-employed couples in their 50s without employer coverage, monthly marketplace premiums of $1,400 to $2,000 are realistic in many markets. These are significant costs that must be factored into business pricing decisions, quarterly estimated tax planning, and overall financial planning from the outset of any self-employment arrangement.

Maximizing Marketplace Subsidy Eligibility

For self-employed individuals whose income is near or below the subsidy eligibility thresholds, understanding how modified adjusted gross income is calculated for ACA subsidy purposes is critically important and often misunderstood. MAGI for ACA purposes includes net self-employment income after business deductions but before the self-employment tax deduction, the self-employed health insurance deduction, and contributions to retirement accounts like SEP-IRAs and solo 401(k) plans.

This means that maximizing retirement account contributions and claiming all legitimate business deductions can reduce the MAGI figure used for subsidy calculation, potentially restoring or increasing subsidy eligibility. A self-employed consultant with $95,000 in gross income who has $20,000 in legitimate business expenses and contributes $20,000 to a SEP-IRA may have a MAGI of approximately $55,000 for subsidy calculation purposes, placing them within the subsidy-eligible range despite substantial gross revenue. This is not tax evasion; it is the proper application of deductions that Congress specifically intended for self-employed taxpayers, producing a real and significant financial benefit when applied correctly with the assistance of a qualified tax professional.

The HDHP Plus HSA Strategy for Self-Employed

Self-employed individuals are perhaps the ideal candidates for the high-deductible health plan plus health savings account combination, for several reinforcing reasons. First, self-employed individuals often face higher effective tax rates than equivalent-income employees because they pay both the employee and employer portions of self-employment taxes, currently 15.3 percent on net self-employment income up to the Social Security wage base. The pre-tax nature of HSA contributions therefore produces larger absolute tax savings for self-employed individuals than for employees contributing the same amount at the same gross income level.

In 2026, a self-employed individual contributing the maximum $4,300 to an individual HSA in the 24 percent federal tax bracket saves $1,032 in federal income taxes plus reduces the base on which self-employment taxes are calculated, producing additional savings. For a family contributing the $8,550 maximum, the combined federal income tax and self-employment tax savings can exceed $2,500 to $3,000 depending on the specific tax situation. Over a career of maximum HSA contributions, the accumulated tax-free balance invested in diversified index funds can become a substantial dedicated fund for healthcare costs in retirement, when healthcare spending typically increases significantly just as employment income ends.

The Self-Employed Health Insurance Tax Deduction

One of the most valuable tax provisions available to self-employed individuals is the self-employed health insurance deduction found at Section 162(l) of the Internal Revenue Code. This deduction allows self-employed individuals, general partners, and more-than-2-percent S corporation shareholders to deduct 100 percent of health, dental, and long-term care insurance premiums paid for themselves, their spouses, and their dependents from their gross income.

Unlike most itemized deductions, the self-employed health insurance deduction is an above-the-line deduction that reduces adjusted gross income regardless of whether you itemize deductions on Schedule A. This makes it valuable even for self-employed individuals who take the standard deduction. At a combined federal and state marginal tax rate of 30 percent, a $12,000 annual health insurance premium produces a $3,600 tax reduction through this deduction alone, meaningfully offsetting the burden of paying full marketplace premiums without an employer contribution.

The deduction cannot exceed the net profit from the business for which the health insurance is established, cannot be claimed for months when the self-employed individual was eligible to participate in a subsidized employer-sponsored plan through a spouse's employer, and cannot be claimed in addition to the ACA premium tax credit for the same premium dollars. These limitations require attention and ideally professional tax guidance, but do not affect the majority of straightforwardly self-employed individuals with no employer-sponsored coverage options available.

Group Coverage Options for Self-Employed

Several organizations facilitate access to group health insurance rates for self-employed individuals who meet membership requirements. Professional associations in fields including medicine, law, accounting, engineering, real estate, and technology frequently negotiate group health insurance programs with major carriers that may offer more favorable rates than individual marketplace coverage. The National Association for the Self-Employed and industry-specific associations in fields ranging from independent journalism to independent trucking often have negotiated group programs. Chambers of commerce in many areas offer small group health insurance programs to member businesses, including sole proprietors.

The value of these programs varies significantly by organization, carrier, and geographic market. Some programs offer genuinely competitive rates comparable to or better than marketplace options for some age and health profiles. Others charge administrative fees that eliminate any premium advantage over direct marketplace plans. Evaluate the total cost including association membership dues and any administrative fees before assuming a group program is more affordable than the marketplace alternatives available to you specifically.

Coverage Through a Spouse's Employer: Often the Best Option

If your spouse or domestic partner has employer-sponsored health insurance that permits family enrollment, this is almost always the most cost-effective health insurance option for a self-employed individual. The employer's contribution to the family premium, which averages approximately $19,000 annually across all employer types for family coverage, represents a substantial subsidy that no individual marketplace plan or group program can match. Even with a meaningful employee contribution to the family premium, the employer plan is typically significantly less expensive than individual marketplace coverage for the self-employed spouse.

One important nuance: if your spouse's employer offers employer-sponsored coverage to you as a family member at an affordable cost, you are considered to have access to affordable coverage and are generally not eligible for ACA marketplace premium tax credits. The affordability determination is based on the cost of adding you to the employer plan as a family member. If the family premium contribution is less than approximately 9.12 percent of your household income, you are typically considered to have access to affordable coverage and lose marketplace subsidy eligibility for the months that offer is available to you.

Special Enrollment Periods for Self-Employed

Self-employed individuals who experience qualifying life events are entitled to a Special Enrollment Period of 60 days on the ACA marketplace. Qualifying events include losing other health coverage, gaining a dependent through birth or adoption, getting married, moving to a new coverage area, and changes in household income that affect subsidy eligibility. These SEP rights mean that self-employed individuals are not locked into annual open enrollment windows and can access marketplace coverage when their circumstances change materially during the year.

For self-employed individuals whose income fluctuates significantly, a change in projected annual income that moves you into or out of subsidy eligibility is itself a qualifying event that allows you to update your marketplace subsidy estimate and make a plan change to optimize your coverage for the new income level. Maintaining accurate income projections and updating the marketplace promptly when your income changes substantially during the year prevents both under-subsidization and the surprise tax reconciliation that occurs when advance premium tax credits exceed the amount you were actually entitled to based on final annual income.

Income Management Strategies for Subsidy Optimization

For self-employed individuals whose income fluctuates year to year, or whose income is near the subsidy eligibility thresholds, proactive income management to maintain or improve subsidy eligibility can produce thousands of dollars in annual healthcare savings. The strategies most relevant to self-employed individuals include maximizing contributions to SEP-IRA or solo 401(k) retirement accounts, which reduce MAGI for subsidy purposes; timing deductible business expenses to coincide with years where controlling income near a subsidy threshold is financially valuable; and structuring major business purchases or investments in years when reducing taxable income has maximum subsidy impact.

The interaction between retirement contributions, business deductions, the self-employed health insurance deduction, and ACA subsidy calculations is complex enough that working with a tax professional who specializes in self-employed client planning is generally worthwhile. The potential annual financial benefit from optimally managing these interactions can easily exceed the cost of professional tax advice, particularly for self-employed individuals with business income near subsidy eligibility thresholds.

What to Budget for Health Insurance as Self-Employed

Self-employed individuals should build health insurance cost estimates into business pricing and financial planning based on realistic income scenarios rather than optimistic assumptions about subsidy eligibility. As a rough planning framework: an individual self-employed person earning $50,000 to $70,000 should budget $200 to $500 per month for marketplace coverage after any remaining subsidy under the original ACA structure. An individual earning $80,000 to $120,000 should budget $500 to $900 per month for marketplace coverage with no subsidy. A family with two self-employed adults and children, earning $120,000 to $180,000, should budget $1,200 to $2,000 per month for comprehensive marketplace coverage with no subsidy in most markets.

Geographic variation is enormous. The same household profile paying $1,200 per month in a competitive urban market with multiple insurer options might pay $2,000 per month in a rural market with limited insurer competition. Using healthcare.gov's plan finder or your state marketplace's quote tool with your actual location, age, and household information produces the most accurate estimates for your specific situation and should be updated annually as premium levels and your personal circumstances change.

Understanding Explanation of Benefits Documents

An Explanation of Benefits document, commonly called an EOB, is the document your health insurer sends after a medical claim is processed. It is not a bill. It is an explanation of how the insurer applied your benefits to the claim submitted by your healthcare provider. Understanding how to read an EOB is essential for verifying that your claims are being processed correctly and for understanding your actual out-of-pocket financial responsibility for any medical service.

The EOB shows several key figures for each service line: the amount billed by the provider, the insurer's allowed amount (the negotiated rate for in-network services or the maximum the insurer considers reasonable for out-of-network services), the amount the insurer paid, and the amount that is your responsibility. The difference between the billed amount and the allowed amount is a contractual writeoff that you do not owe if the provider is in-network; this writeoff represents the benefit of having a negotiated network rate through your insurer.

Your responsibility amount is broken down into deductible applied, coinsurance, and copayment components. This allows you to track your progress toward your deductible and out-of-pocket maximum throughout the year. Many people discover discrepancies between what an EOB shows as their responsibility and what a provider bills them. When this occurs, contact your insurer before paying the provider's bill to verify which amount is correct under your policy terms. Billing errors in medical invoices are common, and the EOB is your authoritative record of what you actually owe.

Preventive Care: What Your Plan Must Cover for Free

Under the Affordable Care Act, all non-grandfathered health insurance plans are required to cover a defined list of preventive services at no cost to the patient when those services are delivered by an in-network provider. This means no copayment, no coinsurance, and the service does not count against your deductible. These covered preventive services include annual wellness visits, many cancer screenings, blood pressure and cholesterol testing, depression screening, immunizations on the CDC recommended schedule, and a range of screenings and counseling services tailored to specific age groups and risk factors.

The no-cost preventive care requirement is one of the most tangible and consistently valuable benefits of ACA-compliant health insurance for generally healthy adults who use medical services primarily for wellness maintenance. A family that takes advantage of all applicable no-cost preventive services receives hundreds of dollars in medical care value annually without any cost-sharing contribution. Understanding which services qualify and using them consistently is particularly important for HDHP enrollees who pay out of pocket for most non-preventive services until the deductible is met.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.