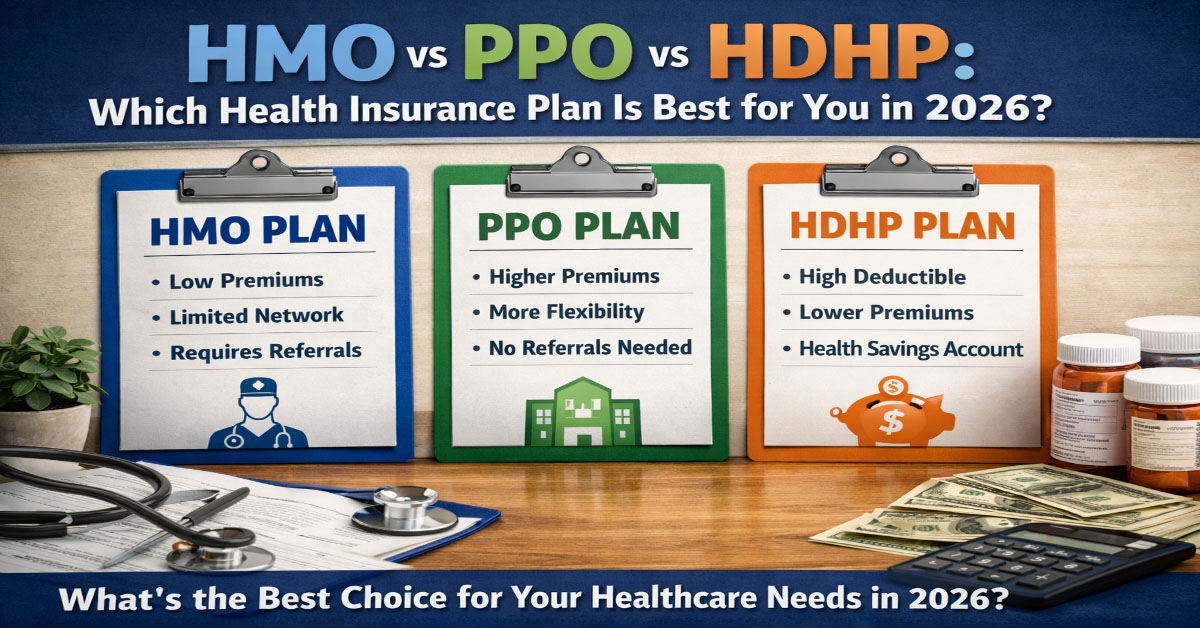

Three letters stand between you and the right health insurance decision: HMO, PPO, and HDHP. Choosing the wrong plan type for your healthcare usage patterns and financial situation can cost thousands of dollars annually, even if the premium looked attractive at enrollment. Choosing correctly can provide comprehensive protection at the lowest sustainable cost for your specific circumstances.

This guide goes beyond standard definitions to give you the analytical framework for making this choice based on your actual healthcare usage, financial position, and risk tolerance. The right answer differs significantly between a healthy 28-year-old, a 45-year-old managing a chronic condition, and a 58-year-old with high specialist utilization. Understanding the structural differences and their real financial implications for your profile is the foundation of a good plan decision.

In This Article

HMO: Health Maintenance Organization

An HMO requires you to select a primary care physician from within the plan's network. This PCP serves as your healthcare gatekeeper: all specialist referrals must flow through your PCP, and most HMOs require a referral before you can see a specialist. Care received from providers outside the plan's network is generally not covered at all, except for genuine emergencies. Emergency care at any facility is typically covered regardless of network status.

The care coordination model is designed around the idea that a primary care physician who knows your complete health history can coordinate your care more effectively and cost-efficiently than a fragmented system where patients self-refer to specialists. For patients with complex multi-specialist care needs, this coordination can genuinely improve outcomes. For patients who primarily need routine care, the referral requirement creates administrative friction without meaningful clinical benefit.

HMOs generally have the lowest monthly premiums of the three plan types. Deductibles are typically low or zero for in-network care. Copayments for routine services are usually modest, often $15 to $30 for primary care visits and $30 to $60 for specialist visits with a referral. The trade-off for these predictable, low cost-sharing amounts is the network restriction: you pay less because you accept a narrower provider choice and a gatekeeper requirement for specialist access.

The HMO is most appropriate for people who want predictable low monthly costs, are comfortable with the network restriction and referral process, and have established provider relationships within the HMO network that they expect to maintain throughout the plan year. For people who value the ability to self-refer to any specialist at any time or who see providers in multiple geographic markets, the HMO's constraints may prove frustrating or costly if non-emergency out-of-network care becomes necessary.

PPO: Preferred Provider Organization

A PPO provides coverage for both in-network and out-of-network care, with meaningfully different cost-sharing between the two tiers. You do not need a primary care physician designation or referrals to see specialists. You can seek care from any provider, any specialist, in any state, at any time, and your coverage will apply, though at a higher out-of-pocket cost for out-of-network care than for in-network care.

The in-network benefit is always the better deal: PPOs negotiate discounted rates with in-network providers, and your cost-sharing percentage applies to that discounted rate. Out-of-network care is covered but at a different, typically higher coinsurance rate, and your cost-sharing applies to the provider's billed charges rather than a negotiated rate. In practice, this can make out-of-network care expensive even though it is technically covered under the policy.

PPOs carry the highest monthly premiums of the three primary plan types. This premium reflects the value of maximum flexibility: you are paying for the option to access any provider, which insurers price as a higher expected payout given the broader and more expensive provider utilization patterns typical of PPO members. Deductibles vary widely but are typically moderate. Separate out-of-pocket maximums often apply for in-network and out-of-network care, meaning total exposure if you use significant out-of-network care can be higher than the in-network maximum alone.

The PPO is most appropriate for people with established relationships with specific specialists or hospitals that may not be in any available HMO or HDHP network, people managing complex multi-specialist chronic conditions who need flexibility beyond any single network's specialist roster, people who travel frequently for work and need reliable coverage in multiple geographic markets, and people who simply value the peace of mind of knowing any provider, anywhere, is covered rather than limited to a defined network.

HDHP: High Deductible Health Plan and the HSA Advantage

An HDHP is defined by IRS criteria based on deductible minimums: at least $1,650 for individual coverage and $3,300 for family coverage in 2026, with out-of-pocket maximums capped at $8,300 for individuals and $16,600 for families. Plans meeting these criteria qualify for Health Savings Account compatibility, which is the primary financial advantage of the HDHP structure over standard HMO or PPO designs.

Under a qualifying HDHP, you pay all medical costs out of pocket until you reach the deductible. After the deductible is met, the plan covers costs at its standard cost-sharing rate until you reach the out-of-pocket maximum. Only preventive services are covered before the deductible under ACA-compliant HDHPs. HDHPs can be structured as either HMO-style plans with network restrictions and gatekeeper requirements, or as PPO-style plans with broader network access. The distinguishing characteristic is the deductible and cost-sharing structure, not the network design.

The ability to contribute to a Health Savings Account is the feature that elevates a qualifying HDHP from simply being a high-deductible plan to being a potentially superior financial strategy for the right enrollee. In 2026, individuals with HDHP coverage can contribute up to $4,300 to an HSA, and families can contribute up to $8,550. These contributions are made with pre-tax dollars, grow tax-free within the account, and can be withdrawn tax-free for any qualified medical expense. This triple tax advantage makes the HSA the most tax-efficient savings vehicle available in the U.S. tax code for healthcare purposes, producing tax savings for every dollar contributed in the current year regardless of whether you use those funds for current or future healthcare expenses.

The HDHP produces the best financial outcomes for generally healthy individuals with few anticipated medical expenses who are in meaningful tax brackets where the deductibility advantage is substantial, who have sufficient financial reserves to absorb the higher out-of-pocket costs if a significant medical event occurs, and who have the discipline to actually fund the HSA rather than simply carrying the HDHP without the savings component that makes it financially superior.

EPO: The Less-Known Middle Option

Exclusive Provider Organization plans combine elements of both HMO and PPO designs in a way that some enrollees find attractive as a middle ground. Like a PPO, an EPO does not require referrals to see specialists. Like an HMO, an EPO does not cover out-of-network care except for emergencies. You can self-refer to any in-network specialist without gatekeeper involvement, but if you go outside the network for a non-emergency, you pay the full cost entirely out of pocket. EPOs are less widely available than HMOs and PPOs but are increasingly offered by major carriers, particularly in employer-sponsored plans. They can be an attractive option for people who want the referral-free flexibility of a PPO but are comfortable with a narrower network restriction and are drawn to a premium that is typically lower than a comparable PPO.

HMO vs PPO vs HDHP: Side-by-Side Comparison

The Total Annual Cost Calculation

The most common mistake in plan selection is focusing on the monthly premium rather than the expected total annual cost. Total annual cost equals twelve times the monthly premium plus expected out-of-pocket spending for your anticipated healthcare utilization pattern. These two components trade off against each other across plan types: lower-premium plans have higher cost-sharing, and higher-premium plans have lower cost-sharing at point of service.

For a healthy adult expecting one preventive visit and perhaps one sick visit per year, the calculation might look like: HDHP premium savings of $150 per month over the PPO equals $1,800 in annual premium savings. Expected out-of-pocket medical costs: $200 under the HDHP versus $50 copay under the PPO for the sick visit. Net HDHP advantage: $1,650 for this utilization pattern. The HDHP wins clearly for this low-utilizer, even before factoring in the HSA tax benefit.

For an adult managing Type 2 diabetes who sees their primary care physician four times per year, a specialist twice per year, and fills multiple prescriptions monthly, the calculation shifts substantially. The HDHP deductible may be reached relatively early in the year as prescription and office visit costs accumulate, but before it is reached, all costs are paid entirely out of pocket at full rates. The HMO's low copayments apply from the first visit. The total annual cost for this utilizer profile frequently favors the HMO or a lower-deductible PPO despite their higher monthly premiums.

Choosing When You Have a Chronic Condition

Chronic condition management fundamentally changes the plan selection calculus in ways that a simple premium comparison misses entirely. The drug formulary, the list of covered medications and their tier placement, is more important than any other plan feature for people with conditions requiring expensive specialty or brand-name medications. A plan with a low premium that places your essential medication on the highest cost tier can cost far more annually than a plan with a higher premium that covers the same medication at a lower tier. Always verify that your specific medications are covered and at what tier in any plan you are seriously considering before completing enrollment.

Network analysis is equally critical for people with established specialist relationships. Losing access to your rheumatologist, oncologist, endocrinologist, or other key specialist because a new plan's network does not include them is a healthcare disruption with potentially serious clinical consequences, not just a financial inconvenience. Verify network inclusion before enrolling, and obtain documented confirmation rather than relying on network directory listings that are not always current and have been known to include providers who no longer accept that specific plan.

Choosing for a Family

Family plan selection adds the complexity of differing healthcare utilization across household members. The family deductible and out-of-pocket maximum structure differs by plan design. Some plans apply separate individual deductibles within the family maximum through what is called an embedded individual deductible structure, while others apply an aggregate family deductible that must be met collectively before the plan begins covering costs for any family member. The embedded individual deductible protects heavy users from being subject to the full family deductible before the plan starts contributing to their individual costs, which is particularly valuable in families where one member has substantially higher healthcare utilization than others.

Families with young children who need regular well-child visits, occasional pediatric sick visits, and possible urgent care or emergency visits benefit from plans with predictable copayments for these common services. The unpredictability of pediatric care needs argues somewhat against an HDHP for families who cannot absorb significant unexpected deductible costs from accessible savings without meaningful financial hardship.

Choosing Between Multiple Employer Plans

When choosing between multiple employer-offered plans, the decision framework is the same as the general analysis but with one additional consideration: the employer's contribution to each plan type may differ. Employers sometimes contribute a higher dollar amount toward HDHP premiums than toward PPO premiums as an incentive to enroll in the more cost-efficient plan type from the employer's perspective. When comparing employer plans, always compare after-employer-contribution premiums and verify whether the employer offers any HSA contribution for HDHP-enrolled employees, which is increasingly common.

An employer HSA contribution of $500 to $1,000 annually, which many employers now offer alongside their HDHP option, significantly improves the financial case for the HDHP by effectively reducing the net deductible you must fund from your own dollars. Include employer HSA contributions in your total annual cost calculation when comparing employer plan options, and factor in the personal tax savings from your own HSA contributions at your marginal tax rate to get a complete picture of the true after-tax cost difference between plans.

Understanding Explanation of Benefits Documents

An Explanation of Benefits document, commonly called an EOB, is the document your health insurer sends after a medical claim is processed. It is not a bill. It is an explanation of how the insurer applied your benefits to the claim submitted by your healthcare provider. Understanding how to read an EOB is essential for verifying that your claims are being processed correctly and for understanding your actual out-of-pocket financial responsibility for any medical service.

The EOB shows several key figures for each service line: the amount billed by the provider, the insurer's allowed amount (the negotiated rate for in-network services or the maximum the insurer considers reasonable for out-of-network services), the amount the insurer paid, and the amount that is your responsibility. The difference between the billed amount and the allowed amount is a contractual writeoff that you do not owe if the provider is in-network; this writeoff represents the benefit of having a negotiated network rate through your insurer.

Your responsibility amount is broken down into deductible applied, coinsurance, and copayment components. This allows you to track your progress toward your deductible and out-of-pocket maximum throughout the year. Many people discover discrepancies between what an EOB shows as their responsibility and what a provider bills them. When this occurs, contact your insurer before paying the provider's bill to verify which amount is correct under your policy terms. Billing errors in medical invoices are common, and the EOB is your authoritative record of what you actually owe.

Preventive Care: What Your Plan Must Cover for Free

Under the Affordable Care Act, all non-grandfathered health insurance plans are required to cover a defined list of preventive services at no cost to the patient when those services are delivered by an in-network provider. This means no copayment, no coinsurance, and the service does not count against your deductible. These covered preventive services include annual wellness visits, many cancer screenings, blood pressure and cholesterol testing, depression screening, immunizations on the CDC recommended schedule, and a range of screenings and counseling services tailored to specific age groups and risk factors.

The no-cost preventive care requirement is one of the most tangible and consistently valuable benefits of ACA-compliant health insurance for generally healthy adults who use medical services primarily for wellness maintenance. A family that takes advantage of all applicable no-cost preventive services receives hundreds of dollars in medical care value annually without any cost-sharing contribution. Understanding which services qualify and using them consistently is particularly important for HDHP enrollees who pay out of pocket for most non-preventive services until the deductible is met.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.