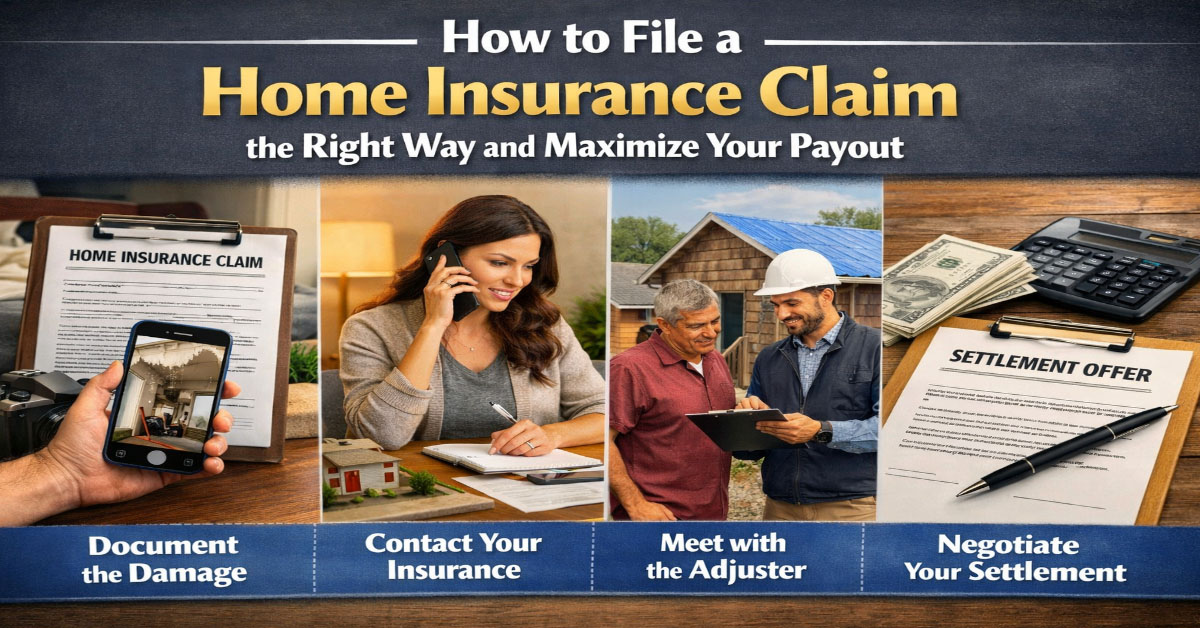

A home insurance claim is a high-stakes financial transaction that most homeowners have never navigated before the moment they need to. The difference between a well-handled claim that produces a fair and complete settlement and a poorly handled one that results in an inadequate payout or a disputed outcome often comes down to how thoroughly and promptly the claim is documented, reported, and managed by the policyholder. You are not at the mercy of the insurance company if you understand the process and your rights within it.

This guide walks through every step of the home insurance claims process from the moment damage occurs through final payment and policy renewal, including what to document, what to say, how to manage the adjuster relationship, and what to do if you believe your claim has been undervalued or wrongly denied.

In This Article

- Immediate Steps After a Loss

- Documentation: The Foundation of Your Claim

- When and How to Report the Claim

- Working With the Insurance Adjuster

- The Repair Estimate Process

- How Settlement Payments Work

- What to Do If Your Claim Is Undervalued or Denied

- When Not to File a Claim

- After the Claim: Rate Impact and Policy Review

Immediate Steps After a Loss

The actions you take in the first hours after a covered loss significantly affect both the total damage outcome and the claim settlement process. Safety is the first priority: if the loss involves fire, structural collapse, gas leaks, or electrical hazards, evacuate the structure and call emergency services before doing anything else. Do not re-enter a structure until it has been cleared as safe by fire department or structural engineering professionals.

Once safety is confirmed, your first priority is mitigating additional damage. Your homeowners policy requires you to take reasonable steps to prevent further damage to covered property after a covered loss. This means covering a damaged roof with a tarp to prevent water intrusion, boarding up broken windows and doors, extracting standing water from a flooded basement, and taking other practical steps to stop the damage from expanding while the claim is being processed. Save all receipts for emergency mitigation work; these costs are typically reimbursable under your additional living expenses coverage or your dwelling coverage.

Do not make permanent repairs or dispose of damaged materials until your insurer has had the opportunity to inspect the damage. Disposing of damaged property before the adjuster can see it may compromise your ability to claim for the full extent of the loss. If damaged materials must be removed for safety or health reasons, photograph and document them thoroughly before removal and retain samples if possible.

Documentation: The Foundation of Your Claim

Thorough documentation is the single most important thing you can do to support a fair and complete claim settlement. The more detailed and organized your documentation, the harder it is for an insurer to question or reduce your claim based on insufficient evidence.

Photograph and video the damage from multiple angles, including wide shots showing the extent and context of the damage, medium shots showing specific damaged areas, and close-up shots showing the specific nature of the damage. If you have pre-loss photographs of the affected areas from any source including old real estate listings, renovation documentation, or personal photos, gather these as well. Before-and-after documentation is more compelling than after-loss documentation alone.

Create a written inventory of every damaged or destroyed item with as much detail as possible: the item description, approximate age, estimated replacement cost, and any documentation you can find such as purchase receipts, credit card statements, photographs of the item, or product packaging. For high-value items, serial numbers and model information are particularly useful. The more specific and quantified your inventory, the better foundation it provides for a complete personal property claim.

Document all expenses incurred as a result of the loss. Hotel costs, restaurant meals above your normal food expenses, emergency home repair and mitigation costs, storage fees for displaced belongings, and any other additional costs resulting directly from the covered loss are potentially reimbursable and should be tracked with receipts from the moment the loss occurs.

When and How to Report the Claim

Report the claim to your insurer promptly after the loss, generally within 24 to 72 hours for significant losses. Most policies require timely reporting, and undue delay in reporting a known loss can complicate the claim process and in extreme cases provide grounds for claim denial. For catastrophic events like fire, report immediately. For slower-developing losses like water damage discovered during renovation, report as soon as you determine the damage is significant enough to potentially exceed your deductible.

Report the claim through your insurer's preferred channel, which is typically the claims hotline, the insurer's mobile app, or their online claims portal. When reporting, provide the basic facts of the loss: the date of loss, the cause of loss, a brief description of the damage, and whether emergency services or temporary repairs have been necessary. Keep the initial report factual and descriptive. You will have ample opportunity to provide detailed documentation throughout the adjustment process.

Request a claim number at the time of reporting and write it down. Every communication with your insurer about the claim should reference this number. Keep a log of every communication including the date, the name of the representative you spoke with, and the substance of the conversation. This documentation becomes important if any disputes arise later about what was said or agreed.

Working With the Insurance Adjuster

The insurance adjuster is the insurer's representative responsible for investigating your claim, assessing the damage, determining coverage, and calculating the settlement offer. Understanding the adjuster's role and how to work effectively with them is important for maximizing your claim outcome.

The adjuster works for your insurer, not for you. Their professional obligation is to determine the appropriate coverage and settlement amount under the policy terms, which may or may not align perfectly with your interests. A competent and fair adjuster will conduct a thorough inspection, document all visible damage, and produce an estimate that reflects what repairs are actually needed. An adjuster who is overworked, inexperienced with your type of loss, or under pressure to limit settlements may produce an initial estimate that understates the actual damage or misapplies policy terms.

Be present during the adjuster's inspection. Walk through the property with the adjuster and point out every item of damage. Do not assume they will find everything; actively direct their attention to damage in areas they might not inspect without prompting, including attics, crawl spaces, and structural areas not immediately visible from a surface inspection. Take your own photographs of every area the adjuster inspects and notes for comparison later.

You are entitled to ask the adjuster to explain any aspect of their assessment and to obtain a copy of their damage estimate after the inspection. Review the estimate carefully and compare it against your own documentation. If the adjuster's estimate misses significant damage items or applies incorrect unit costs for repairs, you have the right to request a revision with supporting documentation.

The Repair Estimate Process

Most insurers will provide an initial repair estimate based on the adjuster's inspection and industry-standard pricing databases. You have the right to obtain your own independent repair estimates from licensed contractors and to use those estimates to negotiate with the insurer if there is a significant discrepancy.

Get at least two to three independent contractor estimates for the repairs. Focus on licensed, experienced contractors who regularly do insurance repair work and who understand the scope documentation process that insurers require. A contractor estimate that is significantly higher than the insurer's estimate is not automatically unreasonable; construction costs vary by market and the insurer's pricing database may not reflect current local labor and material costs.

If your independent contractor estimates are meaningfully higher than the insurer's estimate, present the estimates to your insurer and request a review. Most insurers have a process for reconciling estimate disputes, which may involve the adjuster revisiting the property with the contractor to review specific line items or bringing in a field supervisor for a supplemental inspection.

How Settlement Payments Work

Understanding how insurance payments are structured for your claim type prevents confusion and financial planning mistakes during the repair process. For dwelling coverage claims, the initial payment is typically for the actual cash value of the repair, which represents the replacement cost minus depreciation. After the repairs are completed and you provide documentation of the actual repair costs, the insurer releases the recoverable depreciation holdback to bring the total payment to the full replacement cost value.

This two-payment structure means you may need to fund part of the repair costs upfront or obtain contractor financing while waiting for the RCV payment. Communicate clearly with your contractor about the payment timeline and the two-stage payment process so there is no confusion about when full payment will be available. Mortgage lenders are typically named on the claim check for structural repairs and must endorse the check as a condition of the mortgage, which can add time to the payment process.

For personal property replacement cost claims, the same two-stage structure typically applies: initial actual cash value payment followed by recoverable depreciation payment when you actually purchase replacement items and provide receipts. You generally cannot collect the replacement cost depreciation holdback until you actually purchase replacement items; simply receiving the ACV payment and not replacing the items typically means forfeiting the depreciation holdback portion.

What to Do If Your Claim Is Undervalued or Denied

If you believe your claim has been improperly denied, significantly undervalued, or mishandled, you have several recourse options. The first step is to request a written explanation of the denial or reduction, citing the specific policy provisions that support the insurer's position. Review this explanation against your policy language carefully to determine whether you agree with the application of the policy terms.

If you believe the settlement is inadequate, most policies include an appraisal clause that allows either party to request a formal appraisal process in which each party hires an appraiser and the two appraisers agree on an umpire who resolves any disagreements. This process is distinct from litigation and is often faster and less expensive for resolving valuation disputes.

A public adjuster is an independent adjuster who works on behalf of policyholders rather than insurers. Public adjusters typically charge 10 to 15 percent of the claim settlement as their fee and can be valuable for large, complex claims where the insurer's initial settlement offer is significantly below what the policyholder believes is appropriate. For straightforward claims, the public adjuster fee may not be justified. For large claims with disputed items, the additional settlement a public adjuster secures can significantly exceed their fee.

Your state insurance commissioner's office handles consumer complaints about insurance claims handling. Filing a complaint creates a formal record and prompts regulatory review of the insurer's handling of your claim. For clear coverage disputes that are not resolved through the appraisal process, consulting an attorney who specializes in insurance coverage disputes is appropriate for large claims.

When Not to File a Claim

As discussed in detail in the companion article about insurance versus out-of-pocket repairs, filing a claim for minor losses often costs more in subsequent premium increases than the insurance payout is worth. A general guideline is to avoid filing claims for losses that cost less than two to three times your deductible, particularly for at-fault or maintenance-related incidents that carry higher surcharge risk. Weather-related comprehensive losses like hail and wind damage are somewhat different, as they typically carry lower surcharge risk at most carriers, but the general principle of calculating the full three-to-five year rate impact before filing still applies.

After the Claim: Rate Impact and Policy Review

After the claim is paid and repairs are complete, two important actions are worth taking. First, review your coverage levels to ensure they remain adequate. A significant repair or rebuild project often reveals that your coverage limits were lower than the actual replacement cost, which should prompt a coverage increase to prevent being underinsured for any future loss. Second, request a policy review with your insurer or broker to understand whether and how the claim will affect your premium at renewal, and whether comparison shopping is warranted if a significant surcharge is applied.

Understanding Your Home Insurance Policy's Coverage Sections

A standard homeowners insurance policy is organized into distinct coverage sections, each addressing a different aspect of your financial exposure. Understanding what each section covers and where the limits apply helps you identify potential gaps and make informed decisions about endorsements or supplemental coverage that might be appropriate for your specific property and circumstances.

Coverage A is dwelling coverage, which pays to repair or rebuild the physical structure of your home if it is damaged by a covered peril. The dwelling coverage limit should reflect the estimated cost to rebuild your home from scratch, not its market value or purchase price. Rebuilding cost and market value can diverge significantly, particularly in markets where land values represent a large portion of property value or where construction costs have risen faster than home prices. An annual review of your dwelling coverage limit against current construction cost estimates helps prevent the co-insurance gap that occurs when your coverage limit falls meaningfully below actual rebuilding cost.

Coverage B is other structures coverage, which pays for damage to structures on your property that are not the main dwelling. Detached garages, fences, pools, sheds, and guest houses are all covered under this section. The limit for other structures is typically set at 10 percent of the dwelling coverage amount by default. If you have substantial outbuildings, a detached garage with valuable equipment, or a standalone structure used for a home business, evaluate whether the default 10 percent limit is adequate for your specific property configuration.

Coverage C is personal property coverage, which pays for damage to or theft of your belongings anywhere in the world. The default coverage limit is typically 50 to 70 percent of the dwelling coverage amount. Personal property coverage operates on either a replacement cost value basis or an actual cash value basis. Replacement cost value coverage pays what it costs to buy a new equivalent item. Actual cash value coverage pays the depreciated value of the lost item, which is often substantially less than what it costs to replace it. Upgrading to replacement cost value for personal property is generally worth the additional premium, particularly for households with significant electronics, furniture, and clothing.

Flood Insurance: The Coverage Gap Most Homeowners Do Not Know They Have

Standard homeowners insurance policies explicitly exclude flood damage. This exclusion is one of the most consequential coverage gaps in American property insurance and affects homeowners in every state, not just those in recognized coastal flood zones. Flooding caused by storm surge, rising rivers, overflowing storm drains, heavy rainfall runoff, and snowmelt can all cause catastrophic home damage that is entirely uninsured under a standard homeowners policy.

Flood insurance is available through the National Flood Insurance Program, administered by FEMA, and through a growing number of private flood insurers who entered the market in recent years. NFIP policies provide coverage for the building structure and its foundation, electrical and plumbing systems, HVAC systems, appliances, and the floor coverings and cabinets considered permanently installed. Personal belongings are covered under a separate NFIP personal property policy that must be purchased independently from the building coverage.

The common misconception is that flood insurance is only relevant for properties in FEMA-designated high-risk Special Flood Hazard Areas. In reality, approximately 25 percent of all NFIP claims come from properties outside the highest-risk flood zones. Properties in moderate-risk areas receive lower NFIP premium rates than high-risk areas, making flood coverage more affordable than many homeowners assume. In a state like Texas, where flash flooding affects neighborhoods far from any recognized floodplain on a nearly annual basis, the absence of flood insurance is a significant and common financial vulnerability.

Insurance coverage decisions benefit from regular review because both your circumstances and the insurance market change continuously. Setting a calendar reminder to review your coverage at least 30 days before each renewal gives you time to compare quotes, evaluate coverage changes, and make adjustments based on changes in your financial situation, family structure, or risk exposure. The most effective insurance strategy is not a one-time decision but an ongoing process of alignment between your coverage structure and your actual needs and financial capabilities.